Download StuCred.

The Real Time Student Credit App.

How to Get a ₹20,000 Student Loan in India — Options, Eligibility, Step-by-Step Application and Tips

It is common for students trying to come up with ₹20,000 or so for their upcoming tuition shortfall, exam fees, and the cost of books, or simply a laptop. However, thanks to tailored small-ticket education loans, NBFC and fintech micro-loans via campus tie-ups, and government top-ups — designed to be easier and faster for students to access than large education Loans — now shape India’s lending ecosystem. We guide you through the options and eligibility, how to apply, how interest and repayments work, where to get one, considering affordable lenders, alternative ways of borrowing, and protections so that you can borrow responsibly and build up a credit record.

Why consider a ₹20,000 student loan? It is typically less expensive and takes less time than using credit cards or high-interest personal loans. Many lenders offer quick disbursals for short tenures that fit students’ repayment ability. Just for these times, small loans can fill immediate cash gaps (e.g., library fees, hostel deposits, and course modules), help you seize time-sensitive academic opportunities, and even spread the cost of essentials too.

Search terms to use while comparing offers: 20000 student loan, ₹20000 education loan India, instant student loan 20000, and lastly, fintech education loan 20000/20000 student loans available without a co-applicant in India. Look for lenders that specify the interest rates, processing fees, tenure options, and foreclosure charges. Additionally, see if the lender reports it to CIBIL–you have to repay responsibly (to form a good credit for your future needs.

MUST DO’S: Prepare documents — ID, address proof, admission/ fee invoice, and other academic papers; decide whether a co-applicant is needed or not; prepare a cost break-up and repayment plan within the CASA chart; compare APRs and fees.

The article goes on to cover sections on the types of loans, who should take a loan, eligibility requirements in detail, top-of-the-line lending institutions and platforms around youth, with a step-by-step application process, examples of EMI calculations (to better understand deep borrowing), and alternatives facilitating fraud prevention) and credit-building with relevant case studies, facilities, and local help desks available in major cities. Go through the pertinent sections carefully and choose the most suitable small-ticket student loan option to borrow safely.

Types of ₹20,000 Student Loans Available in India

Short-term education loans vs. long-term student loans

Short-term/small-ticket education loans: Ideal for short-term needs; tenure of 3–24 months with faster approvals and less paperwork. Best suited for top-up of fees, exam charges, Books, laptop purchase, or hostel deposits.

Long-term student loans: Traditional education loans with multi-year tenures for full-course fees, moratoriums, and often require co-applicants or collateral. Not necessary for a ₹20,000 need unless bundled with larger financing.

Bank loans (public sector, private banks) offering small-ticket loans

Public sector banks: Most nationalized banks offer education loans under uniform schemes and with smaller disbursals. It will involve relatively conservative approval criteria, potentially requirements of a co-applicant, and slower processing, even though the terms would be regulated.

Private Banks: Faster processing and digital application journeys (for small loans). They tend to offer flexible tenure options and instant credit decisions for students with co-borrowers or strong CIBIL records, as well as those with check-processing and prepayment fees.

NBFC and fintech micro-education loans

NBFCs and fintechs that disburse instant, small-ticket loans through app partners or other platforms. They usually require at least a few documents (admission proof, fee invoice, ID) and disburse within hours. While it may offer higher interest rates than banks, its advantages lie in convenience, with instant approval and several options, including EMI cards, BNPL, and wallet disbursals.

Risks: Also be vigilant of high APR, hidden fees, and aggressive recovery practices.

Campus-linked loan schemes and college tie-ups

A considerable number of colleges/universities collaborate with banks, NBFCs, or fintechs for campus loans. Such schemes might permit payment of fees directly to the institute, offer largely documentation-free routes, and, in some cases, exemptions from processing fees.

Strengths: ease of use, built-in fee invoicing, and custom tenor/holiday structures that mirror academic terms. Check if the tie-up lender reports payments to credit bureaus.

Government schemes and scholarship top-ups for small amounts

Government scholarship programs and grants may cover part or all of small expenses; also, some state schemes or central portals listing student fee assistance can help reduce loan amounts.

Short-term advances at concessionary interest rates from government-supported schemes are available to cover small residual gaps. Before looking for any scholarships, always check the scholarship desks at your university, then the central/state scholarship portals.

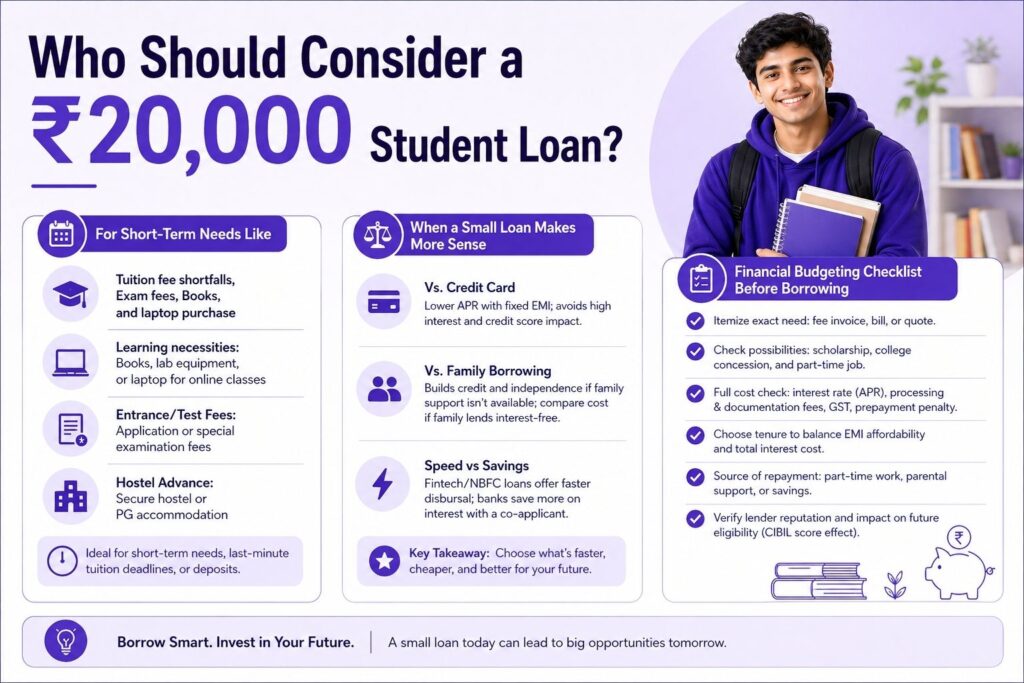

Who Should Consider a ₹20,000 Student Loan?

Tuition fee shortfalls, Exam fees, Books, and laptop purchase for college, Hostel advance

Uses term: short-term needs, the last-minute tuition installment deadline, or deposit

Learning necessities: Purchasing books needed for a course, lab equipment, or a laptop if your degree requires online classes.

Capable/Entrance/Test Fees: Application fees or special examination that should be paid even before taking the entry.

Flated: Hostel or PG advance that secures a room for the semester.

When a small loan makes more sense than a credit card or family borrowing

If you do not have a card or your credit card has a high APR, a small education loan with fixed EMI can still be cheaper and avoid peaks in credit usage that affect your score.

Borrowing from family: If family assistance isn’t available or would strain relationships, a small formal loan builds credit and independence; conversely, if family can lend interest-free, compare the cost and credit benefits.

Speed is much better for fintech/NBFC loans, whereas if you have a co-applicant, banks can save you quite a bit of interest on the same.

Financial budgeting checklist before borrowing

Itemize exact need: fee invoice, bill, or quote.

Check possibilities: scholarship, college concession, and full-time job.

Full cost check: interest rate (APR), processing and documentation fees, possible GST, Polaris penalty for prepayment.

Choose tenure to balance EMI affordability and total interest cost—shorter tenure lowers interest paid but increases EMI.

Source of repayment: working part-time, a bursary from my parents, or savings

Verify the lender’s reputation and if the loan impacts future eligibility (CIBIL score effect)

Eligibility Criteria Specific to India

Eligibility Criteria: Indian resident, Proof of admission, Age, and type of course.

Residency/citizenship: Most lenders require the customer to either be an Indian citizen or a resident

Proof of admission. Almost all student loans require a letter of confirmed admission, an enrollment ID, or a fee invoice from a recognized institute/university as proof, regardless of whether it’s ₹20,000 micro-loans or not.

Eligible Course & institute: The lender will need to recognize the MBA program as a professional/undergraduate/postgraduate diploma, or certification program. Depending on the lender’s policy, each may fall into their short-term skill courses, which may also qualify.

Age restrictions: Usually 18–35 for student loans; for non-adult applicants, a co-borrower (parent/guardian) is required.

Co-applicants and collateral requirements for smaller loans

Co-applicant: While many NBFCs and fintechs for small-ticket loans of, say, ₹20,000 do not require a co-applicant, with banks, the requirement is based on the borrower’s age and course; it could be a parent/guardian as a co-applicant.

Collateral: ₹20,000 loans typically do not require collateral. For small education loans, banks generally do not require collateral. Still, some banks may seek security or a guarantor for applicants with a poor repayment record.

Guarantor versus co-applicant: A co-applicant splits responsibility and is on the documents, while a guarantor backs repayment but is not a co-owner of the loan—terms vary.

Documents required (ID, address, admission/fee invoice, academic records)

Mandatory documents often include:

- Photo ID Proof: Aadhar, PAN, Passport, Voter ID

- Proof of address: Aadhar, utility bill, rental agreement.

- College Admission proof: College admission letter, enrollment letter, or training college invoice for the charge quantity and due date.

- Academic records: Latest marksheet or certificate to provide proof of being a student.

- Bank statements: 3–6 months for the co-applicant/guardian (Some fintechs/NBFCs might not ask)

- Photograph and signature specimen.

Fintech apps: They may only need a couple of documents—digital Aadhaar/e-KYC, an institute invoice, and mobile number OTP verification.

Impact of Income Slabs & CIBIL on Approval for 20,000₹

Comes with fewer income requirements: Since the ticket size is small, normally, the co-applicant’s Income Proof will be requested if the applicant is ultimately a minor or has no credit history. Without admission proof, ehh — NBFCs/fintechs are good to go.

CIBIL and credit scrutiny: For even a ₹20,000 loan, lenders check the credit records of both co-applicants and sometimes the borrower as well. Having a clean or small credit history is fine; however, past defaults or high delinquencies can result in lower approval rates and higher interest charges.

Existing liabilities: How much the co-applicant has to pay out as the outstanding debt-to-income ratio. A heavy burden can make approval less plausible.

Score thresholds: All banks require a CIBIL score>650; however, this may be lower if a co-applicant is involved; on the other hand, fintechs tend to be more flexible but may price risk higher.

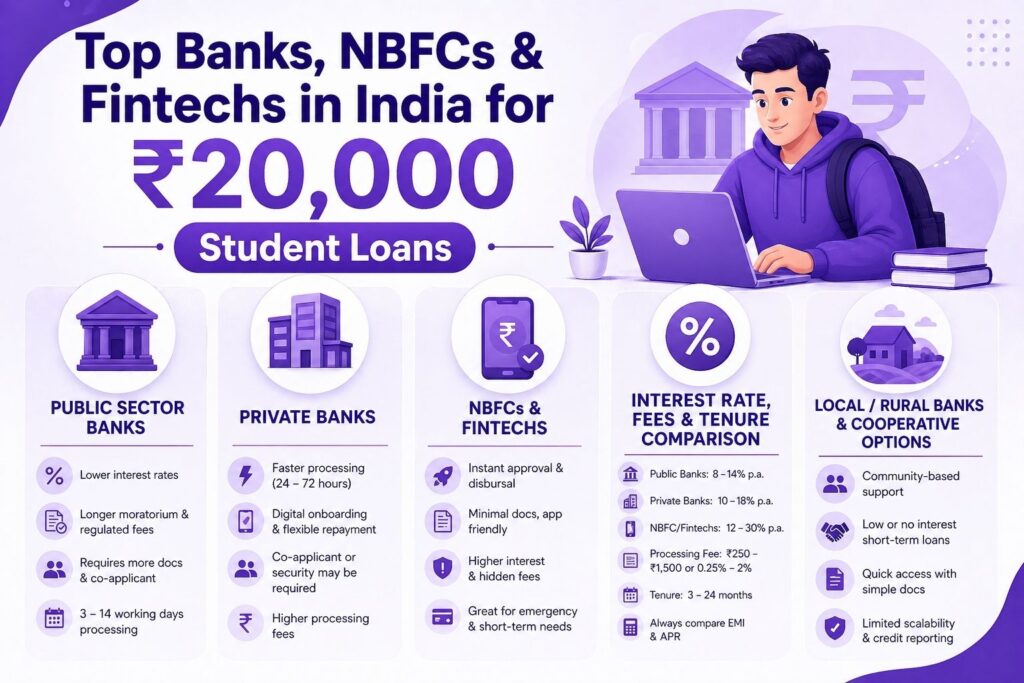

Top Banks, NBFCs, and Fintechs in India for ₹20,000 Student Loans

Public sector banks: typical product features and how to apply

Features:

- Interest rates are lower than those of most private / fintech lenders.

- Standardized products under education loan schemes may offer longer moratorium and regulated fee structures.

- Often requires additional documentation and a co-applicant (parent/guardian) based on the borrower’s profile.

Application process:

- Go to the bank branch or online portal; — Pick the Education loan application.

- Present evidence of admission, invoice for payment, photographic identification, and address proofs – most recently issued documents must be submitted; Proof of co-applicant status.

- KYC, Income verification for Co-applicant + longer timelines for verifications (3–14 working days for small loans)

- Nationalized banks sometimes advertise “education loans for professional/technical courses” — whether these allow small disbursals like ₹20,000; some regional public banks approve student advances with simple rules.

Private banks: faster processing time, varying eligibility

Features:

- Full-fledged digital onboarding, quicker credit decisions, and disbursals windows (often within 24–72 hours)

- Various repayment options, including special deals for students.

- Student credit accounts in overdraft style or short-term bridges;

Application notes:

- Submit the application online or at a branch; open the admission invoice and ID evidence.

- In case of credit, private banks can ask for a co-applicant or security.

- Processing fee comparison: Private banks charge higher fees than public-sector or nationalized banks for small loans.

NBFCs and fintech lenders: instant disbursal apps, benefits, and risks

Benefits:

- KYC within 45 Seconds using OTPs, Fewer documents, Instant decisioning, and instantaneous disbursal of ₹20,000.

- College app-friendly, EMI calculators, tenures from 3–24 months, and tie-ups with college fee portals.

- Few provide “pay later” and EMI card options as a Marketplace for Students.

Risks:

- Interest rates and service charges are higher than those offered by banks.

- Hidden fees, draconian late-payment penalties, and possibly no regulatory clarity—confirm NBFC registration.

Popular use-cases:

- Various payments: emergency fees, online courses fees, equipment purchases

- Look for NBFCs with education-specific products or fintechs partnered with universities.

Interest rate, processing fee, and tenure comparison for a ₹20,000 loan

Interest rates:

Public banks: usually lower (for bigger education loans) but small-ticket rates differ; roughly 8-14% p.a.

Private banks: 10–18% p.a.

NBFC/fintechs: 12–30% p.a. (flat/reducing balance—check APR)

Fees:

- Processing fees, which could be either fixed (₹250–₹1,500) or a percentage (0.25–2%) + convenience fee added by fintechs.

- Compare the documentation fee, GST, and the late-payment charges, etc.

Tenure:

Short tenures (3–24 months) are common for ₹20,000; choose a tenure to balance EMI affordability and interest paid.

Example comparison approach:

- Always compute EMI and total interest (APR) rather than the headline rate.

- For fintech with instant approval, weigh speed vs. interest and fees.

Local/Rural bank and cooperative society options for students

Local banks & cooperatives:

- Sometimes lenient with community scholars, typically supplemental short-term loans or “education loans” up to low amounts, with discretion.

- Sometimes, cooperative societies or student unions provide low- or no-interest loans.

How to access:

Visit the branch; bring the admission invoice and student ID. Local lenders may grant a sanction quickly due to community ties.

Caveats:

Limited scalability, may not report to credit bureaus (impacting credit history), and governance varies—cyber outlook warranty based on inspection.

Step-by-Step Application Process

Pre-application: paperwork, budget plan, co-applicant

Prepare documentation:

- An identity proof, digital fingerprint, passport-size photo.

- Admission letter/enrollment fee and original bill specifying the amount to pay

- Academic certificates/latest marksheet.

- Co-applicant documents: ID, PAN, address proof, 3–6 months’ bank statements, and latest salary slip (if applicable).

Cost breakdown:

- Principal listing (₹20,000); interest fee assumes the selected length, processing/documentation expenses, and GST.

- Choose the right EMI amount and tenure scenario (months — 6 months v/s 12 months).

Co-applicant selection:

- Choosing a parent/guardian with a secure job lessens interest.

- Find out if the lender allows no co-applicant— fintech/NBFCs might allow

Online application guide (common fields and what to upload)

Typical form fields:

- Personal information: name, date of birth (DOB), contact number, email, Aadhaar, or PAN

- Direct admission information: admission number, course name, duration, and fee breakup of the new course & institute.

- Loan Info: amount, preferred tenure, and EMI frequency.

- Co-Applicant Information: details on income, employer, their relationship with you, and contact information.

Upload tips:

- Provide clear scans/photos of the relevant documents (no glare) with high quality.

- Make sure the invoice includes the institute name, the student’s name, and the amount.

- Upload the bank statements in PDF file format that show entries of salary credits, if required

KYC & e-sign:

Aadhaar OTP e-KYC and digital signature (eSign) are used in most of the online flows.

Application process via bank branch/ offline, and what to ask

Branch visit:

- Carry originals and photocopies. Attend the student loan officer meeting or the branch manager meeting.

- Request for a printout of the loan scheme sheet, including the interest rate, processing fee, security requirements, foreclosure conditions, and EMI Schedule.

Questions to ask:

- Specific APR and whether the rate is fixed or variable

- Processing Fee, Documentation fee, GST

- How savings are calculated and Prepayment/foreclosure charges.

- If the lender reports to credit bureaus.

- Timeframe for verification and disbursal.

Negotiation:

Request a processing fee waiver or a rate discount for a co-applicant with good credit (some banks offer concessions for long-term customers)

Timeline: verification, sanction, disbursal

Typical timelines:

Online fintechs/NBFCs: KYC + verification to sanction in mins or 1–2 working days; disbursal same day if docs are in order

Private banks: 24–72 hours, depending on the loan amount, with a co-applicant; some digital products are disbursed within 48 hours.

Local banks: 3–14 functioning days, relying on branch workload and co–applicant verification.

Steps:

Applying for the loan → KYC & document upload → credit/income checking→ sanction letter → acceptance and e-sign→ disbursal to student/college account

Delays:

This is often due to misinformation between documents, invoice clarification, and delays in adding the co-applicant sum.

What are the most common reasons for rejection, and how can they be avoided?

Reasons:

- Incomplete or Ambiguous fee invoice loss

- Poor credit history of the co-applicant or borrower.

- Lack of matching KYC (name/address).

- The co-applicant has a high debt-to-income ratio.

Avoidance tips:

- Check whether the documents you are uploading are clear (invoices must include a student’s name, an institute’s name, and an exact amount).

- Pre-check and, if needed, rectify the co-applicant’s CIBIL score.

- Give up-to-date contact numbers and proof of relationship with the co-applicant.

- Lender: Opt for lenders backed by the institute, or use campus tie-up channels.

- If it gets rejected, request a written reason and make sure that you fix these issues before making a new application.

Interest Rates, Repayment Options, and EMI Examples

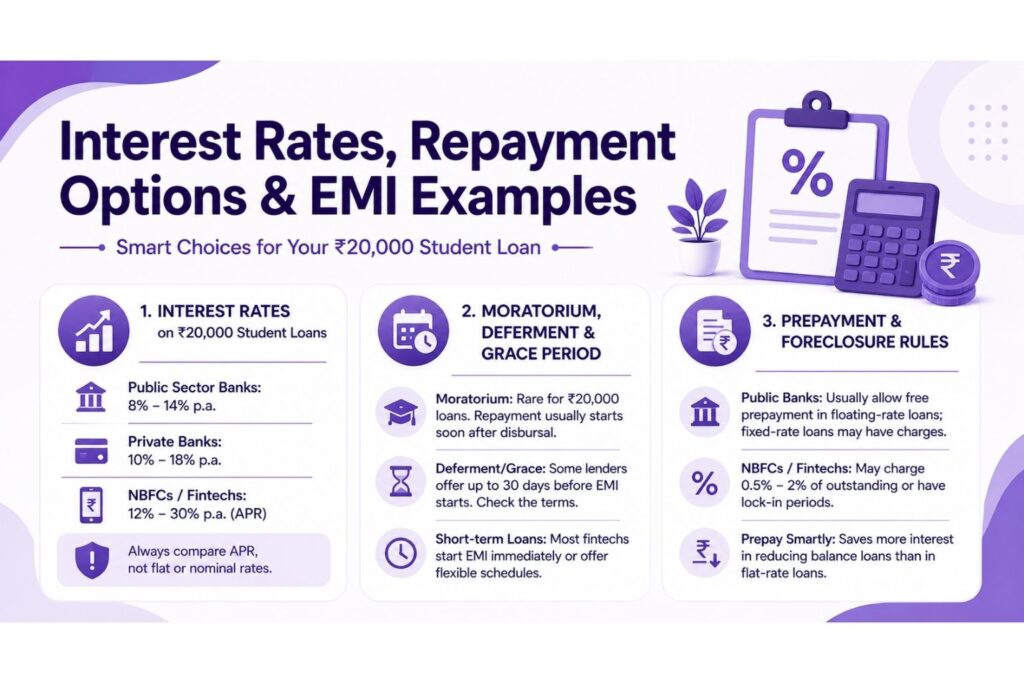

Standard interest rates on student loans of ₹20,000 in India

Range overview:

- Public sector banks: 8–14% p.a. (the reducing balance)

- Private Banks: 10–18% p.a.

- NBFCs/fintechs: 12–30% APR p.a. (may apply flat rates; calculate APR)

Key caution:

Always compare APR and not nominal or flat rates. Apr (actual annual cost) is higher in some fintechs, which otherwise offer a low flat rate.

Factors affecting rate:

Borrower age, co-applicant credit score, type of course, with or without collateral, and special offers.

Understanding the Moratorium, Deferment, and Grace Period

Moratorium:

Generally available on long-term education loans for the course period. Most small-ticket short-term loans (₹20,000) do not have moratoriums—in which case, repayment is almost always within 30–60 days of disbursal or from the first EMI schedule since they are due immediately after a third-party payout is valid;

Deferment/Grace period:

Few lenders give a brief moratorium (up to 30 days) before EMI starts. Verify this in the sanction letter.

Short-term loans:

Most fintech/NBFC micro-loans have immediate EMI starts or flexible monthly/quarterly payment schedules; confirm the position before accepting.

Rules for Small Loans

Bank practices:

Floating-rate education loans offered by public banks allow free prepayment/foreclosure, but be careful with the clause: some public sector banks levy nominal charges for fixed-rate education loans.

Private/fintech:

NBFCs /fintechs may allow for part-prepayment or full foreclosure, but charge (0.5–2% of outstanding) as a fee, or foreclosure may not be permitted within an initial lock-in

Important steps:

Request prepayment terms in writing; evaluate whether a prepayment saves more than the lender’s penalty cost due to lost interest.

A prepayment penalty lowers interest if the lender uses the reducing balance method; for a flat-rate loan, prepayment advantages are minimal.

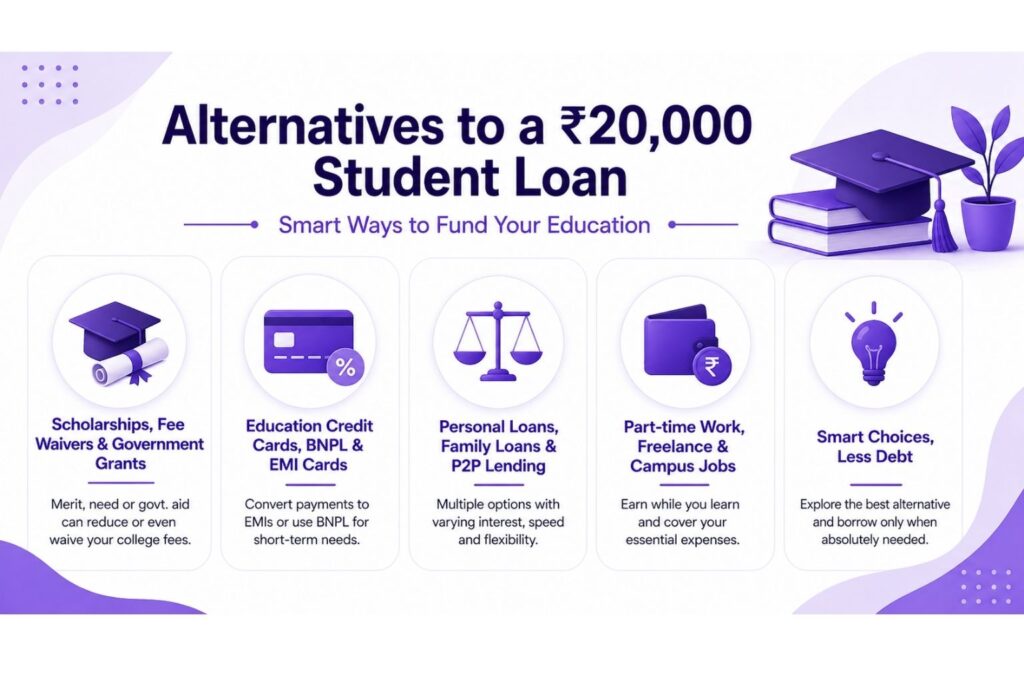

Alternatives to a ₹20,000 Student Loan

Scholarships, Fee Waivers, and Government Grants in India

University scholarships:

Merit-based, need-based,d and college-specific scholarships (scholarships can cover tuition or some other expenses), available online through the financial aid office of a college.

Government scholarships:

Central and state scholarship portals provide funding to eligible students. Check the deadlines, particularly for schemes, as they differ from one institute to another—eligibility ranges.

Fee waivers:

Some colleges offer partial fee waivers, or deferred payments – speak to the accounts office.

Credit cards specific to education, buy-now-pay-later (BNPL), and EMI cards

Education credit/EMI cards:

Some banks/fintechs give education EMI cards enabling the conversion of fee payments into EMIs at stores/shopping portals that are their merchants to avail possibly lower or 0% interest income during the promotional periods

BNPL:

BNPL offers 0 percent interest rates and is typically a short-term loan used to cover equipment or short-course fees — watch for high risk of late payments and limited repayment flexibility.

Use case:

Installment facility reports to the credit bureau and is not included in BNPL, good for small purchases where the net weight of the item is immediate purchase, and repayment is short-term

Pros and Cons of Selected Personal Loans, Family Loans, and Peer-to-Peer Lending

Personal loans:

Fast and unsecured but higher interest than small education loans; usually overkill for ₹20,000.

Family loans:

Generally, interest-free and flexible, which you will want to take advantage of when available. Consider memorializing the repayment terms to avoid disputes.

Peer-to-peer (P2P):

P2P platforms can lend small loans at good rates—consider platform cred and fees

Part-time work, freelance income, and campus earning options

Campus jobs:

Student assistantships, library/lab jobs, and placement-driven internships can cover recurring expenses.

Freelancing:

Tutoring, Content writing, and gigs like a Coding or Microtask → ₹20,000 (in some weeks/months).

Strategy:

Bridge part-time income with a small personal loan; flexible repayments instantly cut EMI and interest load.

Protecting Yourself: Fees, Fine Print, and Credibility Checks

Identifying hidden charges: processing fee, document fee, prepayment penalty

Common hidden charges:

Processing fee (fixed/percentage), documentation fee, digital payments convenience fees, GST on fees, late payment penalty, and foreclosure charges.

How to spot:

Ask for the Fee Schedule and terms statement; total cost (processing + interest + penalties) before acceptance.

Negotiate:

Request fee waivers or reduced processing fees– banks may offer discounts on fees if the applicant is local and applies as a secured loan, e.g., a student, salaried co-applicant in the same bank – so try this route first;

Validating lender credentials and RBI/SEBI/NBFC Registration

Bank as seen in our lives: Public banks, which the RBI regulates, are therefore safe.

NBFCs: must be registered as NBFCs with RBI—confirm via the registration number on the back of the card and verify on the RBI website.

Fintechs: Can tie-up with banks/NBFCs – Check if partner entity is registered; note the terms on which they make their loans (who wins?)

Search:

Company registration, grievance redressal contact, and physical office addresses.

How to read the loan contract, as well as essential clauses to keep an eye on

Clauses to read:

- Interest rate type: whether it is a fixed or floating interest, and calculation basis (flat vs reducing)

- Repayment schedule: EMI date, frequency, and mode.

- Prepayment and foreclosure terms: penalties and lock-in period.

- Penalties for default/late payment and procedures for recovery.

- KYC sharing and privacy: data usage

- Reporting to credit bureaus.

Action:

For every clause, you need a plain-language explanation, the total amount due, an e–sanction letter, and a repayment schedule; also, get it in writing.

Red flags of loan fraud and predatory fintechs

Red flags:

- Lenders Demand Current Processing Payment To A Third-Party Wallet Before Sanction.

- An interest rate that is unclear or inconsistent, with no formal sanction letter

- Heavy-handedness with sales, large penalties not in proportion to the amounts owing.

- No physical address or lack of registration details & no official grievance channel

Safeguards:

Check the lender on the RBI registry, read online reviews, ask for the terms and conditions in writing, and never share your bank details (KYC OTP only).

If in doubt, refer to the college finance cell or get help from government portals.

Building Credit and Financial Planning After the Loan

The impact of timely repayment on the CIBIL score for future loans

Positive impact:

On-time EMI payments go to credit bureaus as data points, strengthening a credit history and increasing the odds of being granted future education or personal loans at better interest rates.

Negative impact:

With a small loan, just 1 missed/late EMI can destroy CIBIL. A default can remain in the records for years and increase the cost of borrowing.

Tip for students: EMI distribution, emergency fund, and savings

Budget priorities:

- Estimate monthly income (part-time job, stipend, parental assistance).

- Pay your EMI first; enable auto-debit to avoid missing it.

- Create a mini-emergency fund (at least one month’s expenses) so you do not have to use high-interest credit if it is depleted.

Sample allocation:

40% essentials (food, commute) — 25% EMI & debt servicing — 15% savings/emergency — 20% study/materials & discretionary. Tweak your distribution based on your situation.

How To Use Small Loans to Build Good Credit Responsibly

Tips:

- Initial tenure must be shorter to pay interest exposure and showcase the fast repayment.

- Credit Limit Management: Avoid maxing out credit facilities; Maintain low levels of utilization.

- Use loans constructively—tuition, buying equipment that makes you more employable — and never to consume.

- Annual credit report monitoring and disputing inaccuracies promptly

Local Resources and Help Desks in Major Indian Cities

Loan assistance cells and a finance officer at the university

- Almost all the colleges have some kind of Student Finance/ Scholarship Cell:

- They keep lists of approved lenders, application forms, and contact people for schemes tied to the campus.

- Student finance officers can refer you to cheap loans, scholarships, and emergency grants—insist on these resources before taking out external loans.

Useful government portals and helplines

- Centralized scholarship portals and Student Financial Aid sections on university websites detail grants and scholarship schemes.

- Special Loan Schemes or Subsidies on the websites of State Education Departments — lookup “government education loan scheme India [Your state name]”.

- You can check the lender’s credentials through the RBI/SEBI/NBFC helplines. These can be used to authenticate the lender to which it is registered and its grievance redressal mechanisms.

Final tips

- Headline rates are often misleading – always compare APRs

- Make the admission invoice & all documents clear and consistent.

- Select lenders that report to credit reporting agencies, allowing you to establish a credit history through timely repayment.

- Prioritize part-time income and scholarships; a ₹20,000 loan should be temporary and used as a gap-filler, not as a long-term fix.