Instant 10000 Loan for Students

#1 Instant Credit App for College Students in India

Empowering Your Financial Freedom

Dear Students,

Welcome to StuCred, your trusted partner in achieving financial independence. We offer instant, interest-free credit designed exclusively for college students across India.

Whether it’s for tuition, textbooks, or day-to-day expenses, StuCred is here to support you. Get an Instant ₹ 10000 Loan for Students

Bharath Reddy

StuCred helped me during my medical emergency. I strongly recommend this app to all the students. Its easy to use and and qiuck to get Money in your bank account

Dhanushiya

The 0% interest is a lifesaver. StuCred has made managing my finances so much easier. It’s an easy way to increase the credit limit as a student.

8Lakh+ students across India are LOVING ❤️ our services. Join the StuCred Community Now!

Why Students Love StuCred

StuCred is more than just a credit app; it’s a trusted partner in student life.

The app is secure, reliable, and designed to cover essential academic expenses, allowing students to focus on their studies without financial stress.

Instant Credit Approval:

The streamlined 5-step verification process means you can get approved for credit in 24 Hours—no lengthy paperwork or waiting periods.

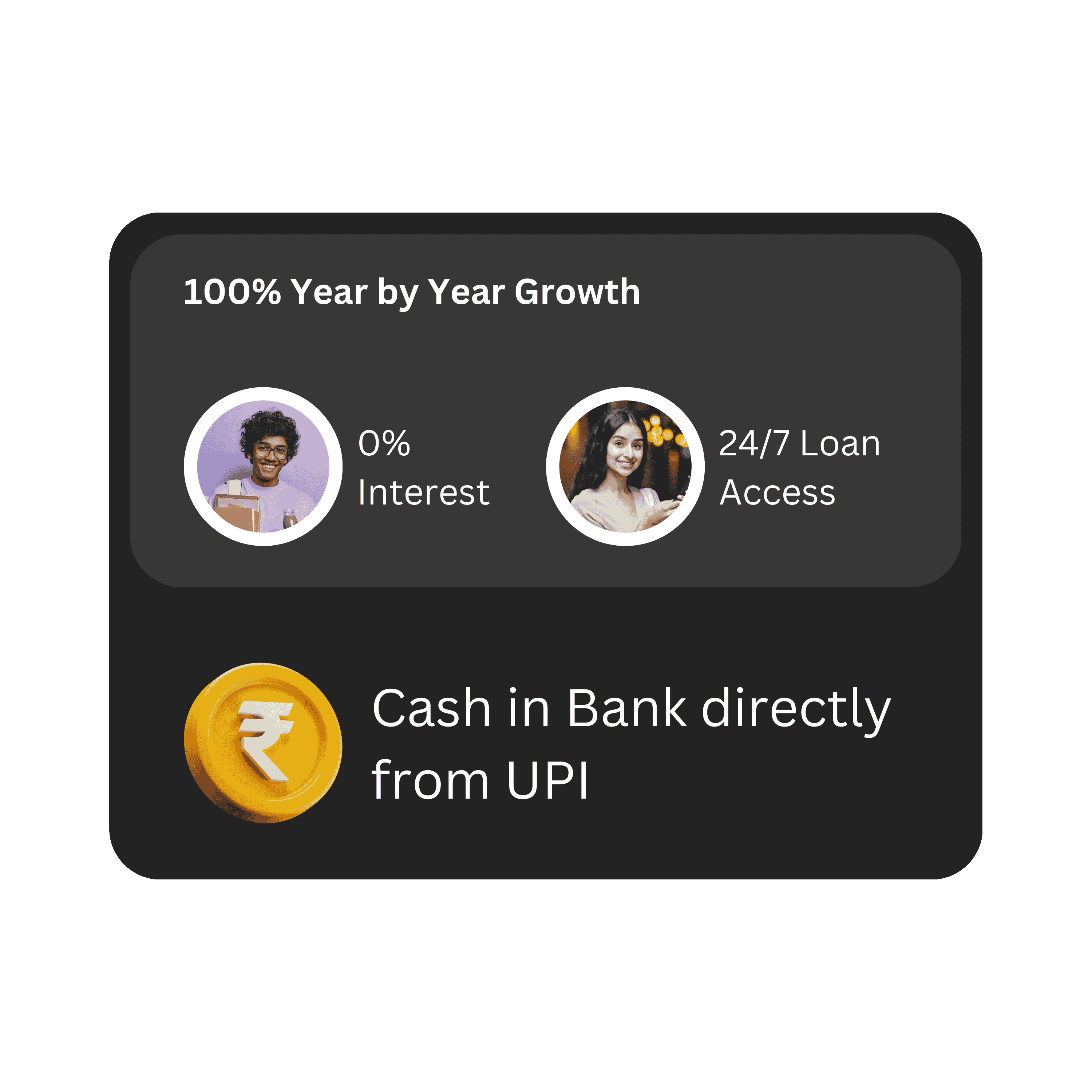

0% Interest:

StuCred offers instant access to credit with absolutely 0% interest, making it easier for students to manage their finances without worrying about extra costs.

Trusted by 8L+ Students:

With a large and growing community of satisfied users across India, StuCred is a name students trust for reliable, hassle-free financial support.

24/7 Loan Access:

Whether it's day or night, StuCred is always there when you need it. Access your credit anytime, anywhere, ensuring you’re never stuck without funds.

How It Works

Fast, Easy, Reliable

Why StuCred?

StuCred offers instant, interest-free credit exclusively for college students in India. With no hidden fees and 24/7 access to funds, StuCred is trusted by over 8L+ students from top institutions.

The app ensures safe, secure transactions with bank-grade security, making it the go-to financial solution for students.

Get Instant ₹ 10000 Loan for Students

No Hidden Fees

Transparent, student-friendly terms. What you see is what you get.

Available Anytime, Anywhere

Get access to your funds 24/7, no matter where you are.

100% Safe & Secure

Your data and transactions are fully protected with bank-grade security.

Trusted by Top Colleges

StuCred is the preferred choice for students from top institutions across India.

Join our Referral Program and Earn ₹5000 Every Month

Click on the link below and get Started

Benifits for Students

With no hidden fees and 24/7 access, students can borrow confidently, knowing they’ll only repay what they borrow.

StuCred ensures funds are always available, making it a convenient and reliable financial solution.

Get Instant ₹ 10000 Loan for Students

Financial Flexibility

StuCred provides students with instant access to interest-free credit, allowing them to manage unexpected expenses, pay for textbooks, or cover daily needs without financial strain.

Stress-Free Borrowing

With no interest and no hidden fees, students can borrow with confidence, knowing they’ll only repay what they borrow, making it easier to stay on top of their finances.

Convenient & Accessible

Available 24/7, StuCred ensures students can access funds anytime, anywhere, whether they need money for academic purposes or personal expenses, ensuring they’re never caught off guard.

31K+ COLLEGES

16L+ HAPPY STUDENTS

24/7 CREDIT ACCESS

8 YEARS OF SERVICE

Download StuCred.

The Real Time Student Credit App.

Instant 10000 Loan for Students

Quick access to financial support can help students handle expenses related to education and daily needs. The ₹10,000 student loan can be considered a small sum that allows students who may not have regular income to pay for immediate out-of-pocket expenses such as textbooks, exam fees, travel, or personal costs. These loans are designed to help students address immediate short-term financial needs without taking on a full-time job or requiring a good credit score.

Taking a loan of ₹10,000 comes with the simplicity factor. While most loans are documented, and primary credit histories are checked before approving loans, student-oriented loans are primarily knowledge-based: they require very little information—sometimes even an Aadhaar card or student ID as validation—and the process is comparatively simple and quick. Some, however, cite a place in the middle class where funds for students have suddenly become available — instant loan apps are mushrooming left and right, as are Aadhaar-linked sanction windows awarding openly without scrutiny within hours [email protected] now asking students to visit offices. As a result, student today can access small loans quickly and focus on their education without financial distractions, compared to the earlier years when getting a loan was never easy.

Mobile apps, online lending platforms, and banks now offer options that students can use to obtain a ₹10,000 loan if needed.

Is it possible for a student to borrow ₹10,000 loan?

Yes, Get an Instant ₹ 10000 Loan for Students, and many financial institutions/loan apps are now offering student loans. These loans are typically easy to qualify, and many don’t require employment verification or credit checks. To be eligible for these sessions, here are the qualification requirements for students —

Eligibility: Lenders generally stipulate that applicants must be at least 18 and enrolled in an accredited school. Additional loan providers may request verification of student status, including a student ID or proof of enrollment.

Documentation: Very little documentation is required. Usually, an Aadhaar card is needed for identification, proof of education, student ID, and basic bank account details for loan disbursement. This makes documentation simple, so students without proof of income or other complicated financial documents can access it.

Popular Lenders: Numerous lenders offer student-friendly, immediate loans. For students, SBI and even Tata Capital provide somewhat snail-paced loans through traditional banking means, while new-age digital-first platforms such as Stucred and MPokket provide instant app-based loan approval exclusively for students.

Category of Loans: Student loans do not require collateral or security, which is a wise option for students with no property. However, certain financial institutions may provide collateralized loan alternatives in case a more substantial loan is required or if someone can cover it using security through an endorser, such as a parent or guardian.

A ₹10,000 loan comes with simple requirements and little paperwork every student can take up easily for this financial solution.

Student Loan Apps for Instant 10000 Loan

The trend of students opting for instant loan apps is rising as they allow fast, simple application and assessment procedures. Students can get loans from platforms that consider them, such as Stucred, ZapMoney, and CredMudra, which do not ask for proof of income or a high credit score or demand extensive documentation.

Advantages: They help students seek loans and get funds in minutes—sometimes, only an Aadhaar card and a student ID are enough. They are very user-friendly, with low documentation requirements and quick processing times. They do not generally require a guarantor, as is the case with conventional loans, but are best suited for independent students.

Cons: Although instant loans are convenient, immediate loans have higher interest rates and less time to return than bank loans. They should study the terms to make sure it suits their capacity.

Bank Loans

For students who want to go the classic lender route, small personal loans from banks like SBI and HDFC are also available. Such loans have lower interest rates than instant loan apps and provide flexible repayment.

Loan Amounts and Repayment: Students can also avail of student loans from ₹10,000 or more with an extended repayment tenure equal to 3–5 years, thus making it easier for every student to repay such loans monthly. Students are offered more flexible repayment terms, and many can get lower rates by applying with a co-signer.

Docs: Banks need standard documents like Aadhaar, proof of enrollment, and, in some cases, even residence proof. Banks generally have low interest rates and customized loan terms, although processing may take longer compared to an instant app.

Steps to get a Student Loan of 10 Thousand Rupees

For students, applying for a ₹10,000 loan is pretty straightforward because many digital lending businesses exist and provide accessible, application-based applications. We use instant loan apps, banks, and government schemes.

For students instant loan apps are best for people who need money within 10 minutes (or) less and do not have time to go through a lengthy process. Here’s how to apply:

Download and Register on App: The first step is to download a reputed loan app such as Stucred, CredMudra, ZapMoney, etc. After installation, register using your phone number or email.

KYC Verification: After registering, you will need to complete the KYC process. Aadhaar verification usually involves uploading an Aadhaar card and a student ID or proof of enrollment. Other apps will require more information, such as bank account details, to transfer funds.

Choose the loan amount (₹10,000) and repayment period you can manage. Loan apps usually provide options for up to 1-3 Months or longer terms.

Double-check that all your information is accurate; less data takes less time to process. After verification, send the application for review.

Disbursement of Loan: Once the loan is approved, the loan amount will usually be disbursed in your bank account in 6 hours or less as it offers a very brief method of availing it.

Bank Application Process

Students who want to follow the traditional way can check for student loans from banks such as SBI, HDFC, etc. Here’s how to apply:

Go to a Local Branch or Use the Online Banking Portals: Applying for these accounts first involves finding your bank and visiting a local branch. Alternatively, you can apply for loans via the portals of the banks that offer them.

Collect Necessary Documents: Banks ask for essential documents like your Aadhaar card, proof of enrollment, and a co-signer if you apply for higher amounts. These documents are also needed if you apply in person. Have them ready to speed up the process.

Eligibility is a Requirement: Banks usually require an eligibility requirement, most likely that you are above 18 and studying at a valid university. A few banks ask for a co-signer if the applicant has no credit history or proof of income.

Submit the Application and Approval: Complete the application form with any necessary documents. Bank loan approvals might take a few days, but they are quick and offer lower interest rates and flexible payments.

Application for Government Schemes

PM Student Loan Scheme 2024 & others are good alternatives for students seeking government-backed loans.

Connection with Bank-used Government Portals: Loans backed by the national government are usually available from partner banks or even within portals specially made for this purpose. For help, refer to the scheme’s official website or check out any of the partner banks’ branches.

You will have to find School letters (which include your 10th scores card, Aadhaar card, and in some cases, parent income proof, etc.) for the parent’s documentation process.

Now, get some applications to file: When all of the documents are ready (make sure you have everything), simply submit an application online or at the partner bank. Government schemes might take a little longer, but the cost of interest remains lower as well and is also adjustable according to the student’s income for repayment.

Digital, bank and government options make it easier than ever to apply for a ₹10,000 student loan. All three methods vary in requirements and processing time, enabling students to select whichever option suits their budget and urgency.

The monthly payment on ₹10,000 Student Loan

If you are a student and want to learn about budgeting, the first step is understanding your monthly payment (EMI) with a 10,000 loan. Monthly installment: the number may vary due to interest rate, loan tenure, and lender-specific terms. Jump to: Overview of how to calculate your monthly payment with a loan calculator and example repayment scenarios across tenures

The formula for EMI calculation is: EMIP×R(1+R)N(1+R)N−1EMI = \frac{P \times R \times (1+R)^N}{(1+R)^N-1}EMI=(1+R)N−1P×R×(1+R)N

where:

P = Loan Principal Amount ₹10000

R = Monthly interest rate (annual interest rate / 12)

N = Loan tenure in months

This formula lets you make monthly payments quickly, considering varied interests and tenure.

Interest Rate and Tenure Options

Each lender offers different rates of interest on student loans for ₹10,000. Banks provide rates between 10% and 15% per annum, while instant loan apps charge a somewhat higher rate, from 15% to 25%, because of quicker processing and limited documentation.

EMI would be approximately ₹3,400 on a 20% annual interest rate for a 3-month tenure.

EMI With a 6-Month Tenure: If the loan amount is extended to 6 months, the EMI will be around ₹1,800.

EMI on 12-month Tenure: If the term extends to 12 months, borrowers will have to pay approximately ₹950 as EMI, making it a much-desirable option for income-stretched students.

Sample Loan Scenarios

Below is an illustration of monthly payments for shorter and longer tenures:

If you select a 3-month tenure with a high interest rate (say, 24%), the EMI will be higher, but your pay-off will be quick. This is the perfect choice if you need cash fast but want to avoid being in debt for years.

Term of Loan: 15% for 12 months. A long-term loan gives you a lower monthly EMI but costs more interest overall. The student may prefer lower monthly payments, so this option helps.

These scenarios and a basic loan calculator can give you an idea of which tenure works for you. A student will most efficiently manage the the₹10,000 loan when they can find the balance between what they can provide to pay a month but which total amount will not only be affordable here and now but also through comparison every penny spent at this price if all students had you borrow each month promptly.

Will I Be Approved for a ₹10,000 Loan If I Do Not Have an Earned Income?

Yes, students can apply for a loan of even ₹10,000 without regular income. Today, many lenders offer students specific financing solutions with relaxed eligibility criteria, like Aadhaar-based verification or proof of enrollment, rather than asking for a salary. So, look at how students find loans without proof of income.

Aadhaar-Based Loans

The process of giving loans based on Aadhaar has made the lending process easy for students, who can apply for a loan quickly with limited documents. Since Aadhaar is the primary identity verification document, along with KYC, digital lending platforms provide loans to students without established employment or salary.

Process in a Nutshell: The central idea of Aadhaar-enabled loans is to identify the borrower (through their unique Aadhaar number), fulfill KYC requirements, and disburse the loan amount. It generally does away with documents such as income proof, salary slips etc.

Advantage: Loans are processed fast without much paperwork or a guarantor, which makes Aadhaar-backed loans an ideal product for the non-salaried segment. These loans are usually unsecured, meaning no collateral needs to be put up.

Loans for Students Without Income. Get Instant ₹ 10000 Loan for Students

Existing financial institutions and lending apps for students provide loans with little to no documentation and without an income requirement. Here are a few of the more popular ones:

Stucred: Stucred is a widely used instant loan platform for students with less paperwork. Loan amount, ₹100 and ₹15,000: Students and the Education Loan can apply using their Aadhaar card and student ID. Stucred is perfect for students without regular income as it does not need proof of income.

CredMudra: CredMudra offers loans for students and young customers. To secure instant funds, students only need an Aadhaar card and proof of enrolment without requiring a salary or a co-signer. Their app-based process is quick and hassle-free so that students can avail of loans in a matter of hours.

ZapMoney: An app-based lender, ZapMoney extends small loans to students based on their Aadhaar and educational status. The loan amount is up to ₹10,000, and the preferred proof of income is zero for students’ short-term cash needs-related expenses.

Other Factors to Make You Eligible for Instant ₹ 10000 Loan for Students

Here are some non-salary factors that improve students’ eligibility — and these build student credentials without a salary:

Academic solid Performance: Few lenders might consider the grades a student gets, seeing high grades as a predictor of future income and responsibility. Thus, a solid academic history can improve the probability of accepting your loan.

Enrollment Confirmation: An important determinant of eligibility is enrollment in a recognized educational institution. To reinforce their commitment to education and career development, students could be required to show proof of enrollment or a student ID card.

Co-Signers: Many lenders do not require this option to make these loans more credible, but in some cases, students should add a co-signer (Mum/Dad/Guardian) to their application because if they are taking out a loan of above ₹10.000, they will most probably ask for one.

Loan up to ₹ 10,000 for Students in India instantly.

In modern india, the world is so fast that students face unexpected financial needs. Cash can be a game changer for purchasing books, traveling, or other daily expenses. This is why instant loans can aid students and are the perfect solution to their instant cash needs. This post explains how instant loans work and the best student platforms.

What is an Instant Loan?

An instant loan is an unsecured loan that offers quick approval and speedy disbursal of the funds, typically without requiring proof such as a credit history or income. These loans are meant to take care of immediate needs, and the whole process is seamless, often happening entirely through mobile apps. Instant loans are a favored option among students who may not have recurring funds but require a small amount funded or just an immediate cash flow for academic or personal use.

Instant Loan: These platforms aim to help you borrow quickly and seamlessly. These types of loans are suitable for emergencies because once you have submitted your application, the loan is typically approved and paid to your bank account within minutes or hours.

Quick Processing Time

All instant loans have fast turnaround times. Unlike traditional loans that can take several days or even weeks to process, instant loans can be approved and disbursed within 24 hours—in some cases, in just a few minutes!

Application: The first step involves completing an application on a lending platform or app, which usually takes two minutes.

Approvals: Platforms generally depend on automated systems to validate your identity and application details, making approval quick.

Disbursement: After approval, the instant loan amount is credited to your registered bank account within an hour or less.

This is a big perk for students who need quick funds in times of need, especially when they experience unforeseen academic or personal expenses.

Instant Loan Apps Services For Students

Here is a list of some student-friendly instant loan platforms in India with their pros and cons:

Stucred:

Stucred sanctions rapid financing to scholars without proof of salary or revenue. Students will find it easier to apply as Aadhaar-based KYC is being used for verification. Instant cash advance: The platform allows flexible loan repayment terms, and loans can be borrowed up to ₹10,000.

The cons are that interest rates can be relatively higher than other traditional bank loans and that the maximum loan amount is limited to ₹10,000, which may not be enough for particular students.

MPokket:

Advantages: One of the instant loan apps popular among students, MPokket provides loans up to ₹10,000 with very little documentation. The app has a quick loan approval process and disburses the funds in a few hours. The interface of MPokket is also user-friendly, and loan payback is possible in easy installments.

Cons: MPokket is convenient but charges exceptionally high interest rates, so students must check if they can comfortably repay.

ZapMoney:

Advantages: Small or education loans are available for students who need proof of the required salary and income. Its mobile app also offers flexible loan periods and an easy application process. You can get the money from a loan in just a few hours.

Cons: The ZapMoney instant loan app consists of elevated curiosity limits, and the mortgage amounts are adequately confined, which is no longer appropriate for massive expenses

How To Get Instant Approval — Tips

Here are a few tips to get your instant loan approved and disbursed immediately.

Be diligent with your KYC: Upload all documents detail-wise—Aadhaar card, student ID, and bank account. Any missing documents or incorrect information may delay the process or cause a denial.

Keep a Clean Credit History: Instant loans usually do not require a credit history, but some platforms still check your credit score to approve or reject the loan. A good credit score will speed up the approval process.

Loans are Disbursed Faster if you apply during business hours. Late-night work and holidays may push your approval to the end of the line.

Keep a Stable Internet Connection: Applications are usually sent through online platforms or mobile applications, so a stable Internet connection helps the application pass without any hindrance.

Best Student Loan Option in India

With so many lenders, terms, and conditions available to choose from, it becomes a task for students in India to compare loans best. From instant loans for everyday purposes to educational expenses, fixed points like interest rates, eligibility criteria, documentation, and repayment flexibility must be considered. So here is a comparison between India’s top student loan providers, including SBI, CredMudra, MPokket, and Zapmone.

Top Providers: A Comparative Analysis

SBI Student Loans:

Interest rates: SBI is among the institutions with some of the lowest interest rates, starting at 10-12 percent pa for student loans.

Documentation: SBI, being a traditional bank, will ask for the following documentation: proof of admission, co-signer (in most cases, a parent or guardian), and income proof of the co-signer.

Processing Time: Approval takes 1-2 weeks as it will require verification of multiple documents and other creditworthiness.

Repayment Flexibility: SBI offers long loan repayment tenures of up to 15 years, offering students ample time to start repaying the loan once they complete their studies.

CredMudra:

Interest Rates: CredMudra provides customers with interest rates ranging from 15–20% per annum, which can be pretty high compared to traditional bank loans, which tend well only for short-term loans.

Process: The process is more straightforward; only an Aadhaar card and enrollment in an educational institution registered with the National Academic Depository. This makes it an excellent option for students who still need to receive a salary, as income verification is required.

Speed of Approval: The loan is approved and disbursed within 24–48 hours, offering a quick solution to immediate financial requirements.

Flexible repayment: Depending on the loan size, CredMudra offers flexible repayment periods of 3 to 12 months.

MPokket:

Interest Rates: While MPokket interest rates are higher at 20-25%, they are comparable with banks’ rates, so the trade-off between price and convenience/speed still holds true here.

There is no need for much documentation for MPokket; you only require the Aaadhar card and student ID. Application for this visa does not require proof of salary or income, making it an ideal student-friendly visa.

Approval Time: MPokket offers ultra-fast loan disbursements. A smart, simple loan can be approved and transferred to your account in minutes or hours.

Flexible Repayment: MPokket provides short-term loans with flexible repayment plans. The loans are to be paid within 3 – 6 months.

ZapMoney:

Interest Rates: ZapMoney loans’ interest rates of 18-22% p.a. are only slightly lower than those of most other instant loan apps.

Minimal Documentation: Like MPokket, ZapMoney does not require much documentation, such as an Aadhaar card and proof of enrollment. It does not require the payment of any wages, and it is available to every student.

Time to Approval: The loan is very fast-tracked, and customers receive their loans in hours, making it suitable for students who need money urgently.

Easy Repayment: ZapMoney has a flexible repayment plan, usually between 3 and 6 months. Because of its short tenure and higher interest rate, it is ideal for small, short-term loans.

Factors to Consider

Here are vital things to consider in selecting the best loan for students: Get Instant ₹ 10000 Loan for Students

Interest rates: A higher amount of interest will increase the net payable amount. While traditional banks such as SBI provide lower interest rates, they may need to process your loan more quickly and document more paperwork. Although instant loan apps such as MPokket and ZapMoney have high interest rates, they provide swift access to these loans.

Repaying the Loans: Repayment flexibility is essential as a student may need a more stable income. SBI provides longer repayment tenures for more significant loan amounts, while instant loan apps have shorter tenures, which makes it easier to access funds quickly.

Eligibility Conditions: For those without a regular income, app-based lenders like CredMudra, MPokket, and ZapMoney are more accessible since they do not require income proof. SBI and other banks, on the other hand, prefer a bank co-signer and additional documents.

Processing Fees: Look for hidden fees like processing, late, and prepayment penalties. Although SBI applies for more extended processing fees, digital platforms such as CredMudra offer much lower processing fees, making them an economical borrowing alternative for borrowers applying for smaller amounts or loans associated with higher interest rates.

Student-Specific Loan Options

Some students need a loan to pay for their tuition fees, and some need it for day-to-day expenses, so Indian ministries have designed these types of loans to fill in such financial gaps. Such borrowers are particularly students, and platforms, including MPokket, CredMudra, and ZapMoney, offer loans with no income proof required and a flexible repayment schedule. These loans are handy since many students may need the funds urgently, and others may not have access to a conventional bank loan.

Banks That Give Loans to 18-Year-Olds

Now that you are a young adult headed toward adulthood, one of your first major financial responsibilities will be handling credit and understanding loans. While loans are available from age 18, individual banks will have different policies about whether to lend money to first-time borrowers. Most loan lenders set a minimum age of 18, but others are more rigid. Here, we discuss how banks and financial institutions are addressing young borrowers in terms of documenting and special conditions for an 18-year-old.

Young Borrower Bank Policies

Most banks in India define the minimum age to obtain a personal or student loan at 18. This age threshold exists because you are considered an adult at 18 and can enter contracts. However, financial institutions are regarded since the youth may not have any credit record or lack of stable income. That’s why, in most cases, banks usually wanted further paperwork and often a co-signed, whether a parent or guardian, to back up the loan being applied to.

Young borrowers might be required to limit the loan amount and pay it back over the years. Most banks and loan providers also have small short-term loans for people over 21 years of age or as set aside by the lender, but the interest rate may be a little higher compared to other older borrowers with external credit lines. Approval may also take into account educational background, previous academic performance, and family financial situation.

Bank Accounts for Students Aged 18 and Above

Many large banks and national financial institutions in India provide loan choices for college children and younger adults from 18 years of age. Let’s take a look at a few:

State Bank of India (SBI):

Who is Eligible: SBI education loans are for Indian students aged 18 who have secured admission to an institution approved by the bank. The loan is available for paying tuition fees, the cost of living, and other study costs.

Amount of the Loan: A bank provides loan amounts from ₹10,000 to 10 lakhs for students studying in India and more than that for abroad studies.

Documents: Proof of admission, KYC docs, and the co-signer (if a student does not make any income) and collateral for more significant amounts. The student must also hold an SBI Bank Account.

Repayment: SBI offers flexibility on the repayment part and moratorium period (the loan repayment period will start after course completion).

HDFC Bank:

HDFC Bank provides student loans at 18 if you are looking for an education loan within the country where a student works toward his studies and is approved to recognize an institution of learning.

Amount of the loan: The loan can be between ₹50,000 to ₹40 lakhs depending on the course and eligibility of a student and whether it is a domestic or international course.

The bank will ask you to submit essential required documents such as an Aadhaar card, university admission proof, and income proof from a co-signer if the student has an active income source.

Easy payment: HDFC Bank offers convenient payments of up to 15 years and the option of flexible repayment after course completion.

Axis Bank:

Eligibility: The student should be over 18 and enrolling in a graduation or post-graduation course. The bank also offers personal loans aimed at young borrowers.

Maximum Loan Amount: The maximum loan amount for higher education varies with the course and institution (but it can be up to ₹75 lakhs)

Documents Required: Proof of Admission, KYC Document, Financial details of the co-applicant if a student doesn’t have any source of income

Repayment: Flexible repayment schedule and moratorium period during course duration.

ICICI Bank:

ICICI Bank also offers personal loans to 18-year-olds, but they need a good credit history (if a co-signer or parent guarantees the loan). It also makes educational loans with lower documentation.

Loan Amount: These personal loans for youth can be up to ₹20 lakhs, depending upon eligibility and loan type at ICICI.

Documentation Young applicants to ICICI need only basic KYC documents and proof of enrolment. Co-applicants may be needed for students who do not earn a steady income.

Tenure: ICICI allows you to choose a tenure between 12 months and 5 years for personal loans so that you have flexibility while repaying.

Supporting Documentation and Collateral

Documentation Requirements for 18-Year-Old Borrowers

Identity Verification: Either an Aadhaar card/ Passport/ Driving License as proof of identity

Age Confirmation — An Aadhaar card or birth certificate is checked to ensure the borrower is above 18.

Proof of Enrollment: Banks ask for evidence that the applicant is enrolled with a recognized educational institute, such as an admission letter or a fee receipt, to obtain education loans.

Income Proof—As most 18-year-olds do not have a regular source of income, banks generally need one to be nominated (generally the parent or guardian) along with salary slips and tax returns for proof of income.

Collateral: Few banks require you to pledge collateral (property, fixed deposit, or insurance policy) for loans of significantly higher amounts. On the contrary, banks generally provide unsecured loans for small education or personal loans.

Conclusion

In today’s fast-paced world, there is always uncertainty since students may suddenly need funds for their fee payment, living expenses, or essential study materials. A small ₹10,000 can do wonders in such dilemmas. Yet, it is necessary to know — what you qualify for, which loans are available, and who offers them best in class based on students.

Some of the essential takeaways from this guide are the different loan types, ranging from instant loan apps such as Stucred and CredMudra to banks such as SBI and HDFC. They offer fast loans, providing loans with little documentation and need at worst an Aadhar card or student ID. Nevertheless, you should compare interest rates, processing fees, and repayment terms to determine the best option.

Going for a loan might relieve you from the pressure of a broken budget, but it is essential to borrow cautiously. Read: Be informed about the interest rates and EMIs payable monthly so you can repay the loan comfortably. Don’t over-borrow; only take out loans that you have the means to pay back on time. Having a clear repayment plan and being aware of due dates are ways to manage your finances organizationally and avoid paying for extra debt.

When used correctly and with intelligent choices behind their use, student loans can become a tool that helps students address income streams short on cash while maintaining healthy long-term finances.

Frequently Asked Questions (FAQs)

The ₹10,000 student loan is an instant personal loan you can get for your urgent financial requirements as a student. It can pay for tuition fees or reading resources but also expenditures needed during the day. Such loans usually come from banks, financial institutions, and even loan apps with low paperwork and faster processing times.

Does the student need a loan of ₹10,000?

Can students above 18 get a loan of ₹10,000? However, that varies based on the lender. Usually, students must be enrolled in an accredited institution and provide documentation such as an Aadhar card, proof of enrollment, and documents of co-signing (a working parent or guardian) if the aspirant doesn’t have a steady income.

Quick ways to get a ₹10,000 loan for students

Students needing an urgent ₹10,000 loan can create an app using instant loan apps like Stucred, CredMudra, or ZapMoney. These solutions provide quick processing and fast disbursement of funds. The documents you need to apply are minimal (Aadhaar card, Student ID, and proof of enrollment). It is easy to get. Funding can sometimes occur within a few hours.

What documents are required to apply for a ₹10,000 loan for students?

Here is the essential Document you require:

Identity document: Aadhaar card or any other ID issued by the government.

Proof of enrollment (student ID or admission notification letter)

Account number for loan disbursement If the student has no regular income, some lenders want co-signer financial documents that do.

How to get a ₹10,000 loan without a salary?

Students can avail of a loan of ₹10,000 without having it as their salary. You only need proof of income to apply for loans with banks. Many instant loan apps and student loan providers are careless or don’t care about that. Instead, they will probably provide Aadhaar-based loans or grant loans based on academic and admission participation in the direction of a university. MPokket and CredMudra are a few platforms that lend money without looking for student income.

What are the top loan applications for students to obtain ₹ 10,000 loan immediately?

Here are some of the best student loan apps for ₹10,000 loans urgently:

Stucred: Provides instant loans with the least documentation processed.

CredMudra: Offers fast loans to students without any need for income documentation.

ZapMoney offers instant loans for small, urgent needs. They provide near-instant cash, usually within a few hours, and have liberal eligibility requirements.

How much can a student get with a ₹10,000 loan?

For example, ₹10,000 personal loan is the amount students can avail of, but it can vary from one lender to another and depend on other factors that define whether or not a student qualifies for the same. While some platforms might give you loans starting at ₹1,000, some might stretch up to as much as ₹10,000 or beyond based on your academic performance and whether you’re already signed up.

If you take out a student loan of ₹10,000, What is the interest rate?

Lenders charge different interest rates on their ₹10,000 student loans. In general, the interest rates for instant loan apps are higher than those for banks simply because the loans are disbursed quickly with hardly any paperwork. When it comes to immediate loans, expect interest rates around 15%-30% every year; for bank loans, it is generally lower—between 10%-15%.

How much can I borrow on an Aadhaar card?

Are there instant loan apps that give ₹10,000 Loans based on an Aadhaar card? Such loans are usually income-proof-free, and the only verification needed is through the individual’s Aadhaar card. MPokket and CredMudra offer instant loans using Aadhaar authentication.

How to increase the chances of getting a ₹10,000 loan approval as a Student?

The following tips will help you improve your chances of getting approved for a loan.

You correctly submit your KYC with valid documents.

Update your Aadhaar card and student ID details.

You can also provide proof of income for your co-signer if this increases your eligibility.

Pick a lender specializing in student loans or one that provides immediate loans for young adults whose income is optional to be given.

All you need to know about paying back a ₹10,000 loan as a Student

We know ₹10,000 is a small amount and can be paid back quickly with time. It all depends on your loan type and your lender’s terms. The EMI (Equated Monthly Installment) option can be availed to return the loan amount in monthly installments over a few months, usually between 3 and 12 months. The borrower must now pay the principal portion and interest regularly every month. Staying on top of the deadlines is essential because if you fail to pay promptly, you risk incurring fees or ruining credit scores.