Student Loan App without PAN Card

#1 Instant Credit App for College Students in India

Empowering Your Financial Freedom

Dear Students,

Welcome to StuCred, your trusted partner in achieving financial independence. We offer instant, interest-free credit designed exclusively for college students across India.

Whether it’s for tuition, textbooks, or day-to-day expenses, StuCred is here to support you.

Bharath Reddy

StuCred helped me during my medical emergency. I strongly recommend this app to all the students. Its easy to use and and qiuck to get Money in your bank account

Dhanushiya

The 0% interest is a lifesaver. StuCred has made managing my finances so much easier. It’s an easy way to increase the credit limit as a student.

8Lakh+ students across India are LOVING ❤️ our services. Join the StuCred Community Now!

Why Students Love StuCred

StuCred is more than just a credit app; it’s a trusted partner in student life.

The app is secure, reliable, and designed to cover essential academic expenses, allowing students to focus on their studies without financial stress.

Instant Credit Approval:

The streamlined 5-step verification process means you can get approved for credit in 24 Hours—no lengthy paperwork or waiting periods.

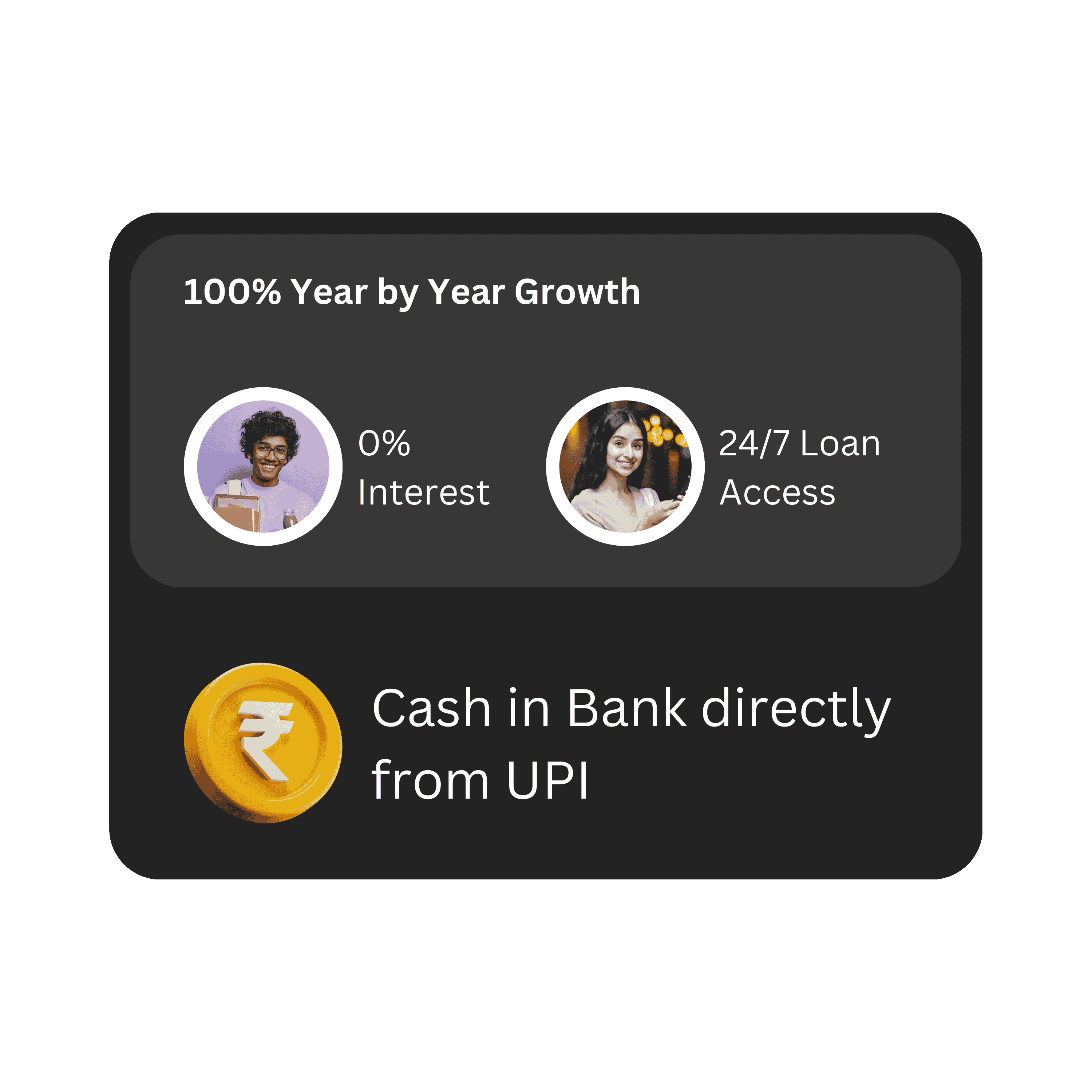

0% Interest:

StuCred offers instant access to credit with absolutely 0% interest, making it easier for students to manage their finances without worrying about extra costs.

Trusted by 8L+ Students:

With a large and growing community of satisfied users across India, StuCred is a name students trust for reliable, hassle-free financial support.

24/7 Loan Access:

Whether it's day or night, StuCred is always there when you need it. Access your credit anytime, anywhere, ensuring you’re never stuck without funds.

Benifits for Students

With no hidden fees and 24/7 access, students can borrow confidently, knowing they’ll only repay what they borrow.

StuCred ensures funds are always available, making it a convenient and reliable financial solution.

Financial Flexibility

StuCred provides students with instant access to interest-free credit, allowing them to manage unexpected expenses, pay for textbooks, or cover daily needs without financial strain.

Stress-Free Borrowing

With no interest and no hidden fees, students can borrow with confidence, knowing they’ll only repay what they borrow, making it easier to stay on top of their finances.

Convenient & Accessible

Available 24/7, StuCred ensures students can access funds anytime, anywhere, whether they need money for academic purposes or personal expenses, ensuring they’re never caught off guard.

31K+ COLLEGES

16L+ HAPPY STUDENTS

24/7 CREDIT ACCESS

8 YEARS OF SERVICE

Download StuCred.

The Real Time Student Credit App.

Student Loan App without PAN Card

What Is a Loan Without a PAN Card in India?

Student financing has always been subject to strict documentation requirements, which often makes it difficult for youth without essential financial documents, i.e., PAN cards, to avail of a loan. But now, with digital lending platforms offering student loan products without PAN cards, this has changed. This policy article elaborates on how a student can avail of loan apps in India without a PAN card and focuses on the alternatives and critical information available for a young borrower.

What does PAN Card mean, and when do you need it for loans?

The Permanent Account Number (PAN) is one of the unique 10-character alphanumeric identifiers the Indian Income Tax Department has issued. It is mainly used to connect any financial operation that must be reported—tax filing, income, and transaction declarations—and large-scale operations like real estate transactions with the citizen’s or entity’s taxpayer account. A PAN card is usually essential when performing almost all financial activities, such as opening a bank account, buying any asset, or applying for a loan above specified limits.

Here, the PAN card acts as an essential document in the loan application process for:

Income Proof: The PAN card verifies the borrower’s income status, which is crucial for credit approval.

Tracking Tax: It ensures the accurate reporting of all financial transactions with taxable implications.

Establishment of Identity: This helps Financial institutions verify the applicant’s identity, thus reducing the chances of data fraud.

For most traditional loans, many lenders use PAN for screening and eligibility checks, so the absence of a PAN card limits the options available to borrowers. However, several loan apps have amended their criteria to target segments such as students who may not have a PAN card by letting them apply for loans with documents like an Aadhaar card.

Why Many Students Lack a PAN Card

There are several reasons why thousands of students do not have PAN cards, making it difficult to avail of traditional credit:

Age Limitations: Most students are under 18, which is the minimum age for getting a PAN card individually.

Income Dependency: Most students depend on their parents rather than earn a taxable income, so the PAN card is not urgently required.

No Formal Employment: Since most students do not work formally, they do not need a PAN as there will be no income and tax. Hence, the requirement to apply for a PAN card is restricted to earning or monetary needs higher than an average student’s expenses.

Thus, students may consider obtaining their PAN card impractical or unnecessary early. This can become an obstacle whenever they require financial aid to cover academic and non-academic needs, creating a need for alternative means that align with their specific situations.

Why is it Crucial to Have Alternatives

Students can be under considerable financial pressures, but they tend to be temporary and short-term—like paying for unexpected expenses, buying textbooks, or other school-related costs (tuition). These expenses are integral to the student’s life, so some different type of loan without depending on PAN card verification has to exist. In such circumstances, PAN-less loan options are crucial when a more accessible option that provides students with rapid financial assistance without the hassle of paperwork is necessary.

Advantages of PAN less Loan Options to the Students:

Easy Accessibility: No official income or tax documentation is required from students.

Quickness: These quick money lending apps prepare funds quickly and are thus suitable for emergencies.

Simplicity in Application: Most PAN-less loan apps have simplified processes and are more oriented towards ease and convenience for younger users.

Existence of Loan Apps in India without PAN

With the emergence of digital lending technology, many financial institutions and fintech companies have developed loan apps that dispense student loans without needing a PAN card. Such apps are student-specific and provide flexibility with less demand for document submission. They often accept the Aadhaar card as the only identity document and do not need any other documents.

Typical PAN-less loan apps offered to students in India include —

True Balance: True Balance is famous for its micro-loan facility; it grants you movable ownership above small sums, with no PAN card necessary. It is perfect for students who need money immediately with the least paperwork

MoneyView: MoneyView allows Aadhaar-based verification for personal loans with flexible tenures (1 yr-7 yrs). The popularity of this applies to the transparent process and student-friendly terms.

Bajaj Finserv: It provides a wide array of financial products and usually asks for PAN while offering higher amounts. Still, small loans can be disbursed without verifying the applicant through the credentials entered and Aadhaar.

Airtel Loans: Airtel has a lending app for applying for loans where Aadhaar-based applications are available. Those deals offer rapid processing, which is a suitable option for students who don’t have a PAN.

Zype and Tata Capital: These apps provide loans specifically for customers without a PAN card. In other words, they offer fast and small loans to help users satisfy their daily expenditures, especially college students.

Such apps facilitate no-nonsense applications to give students access to funds without requiring a PAN card, using alternatives such as Aadhaar as an identification document. The list of PAN-less loan apps is intended for younger, credit-worthy borrowers so they can avail themselves of the required funds to finance their education without any unwarranted pillows.

Why Students Might Need a Loan without a PAN Card

Numerous students find themselves requiring temporary financial support for academic and lifestyle costs. Even though a PAN card is needed to apply for traditional loans, the fact that not all students have it at hand can hinder access to formal credit. What is a PAN Card and Why it Matters to StudentsIn this section, we will look into the financial needs of students in particular, why they find it difficult to avail of loans when there is no PAN card involved, and what alternate options that can plug the gap between money needed.

Financial Needs of Students

The student lifestyle has a few fundamental costs, which can quickly become fitness burdens if a student lives away from home or enters an indispensable situation. Here are some of the most common reasons that students might require financial support:

Academic Costs

Tuition Fees: Tuition fees are often a significant financial burden for students. Scholarships and financial aid are available, but funding is often scarce or competitive.

Academic material: Textbooks, notebooks, software subscriptions, and other study supplies can add up quickly. These are usually unforeseen costs that can immediately burden students financially.

Writing about exam fees and project costs: Some programs require students to pay for examinations or projects, so quick cash is needed.

This includes lifestyles and emergency funds for those who live away from home.

Hostels or Rental Accommodation: Most students live in hostels or rented accommodation, so they spend money on monthly rent, utility bills, and daily living expenses. Being out of state and away from parental assistance makes these costs challenging.

Some students may face medical emergencies and complications, which can lead to them needing instant money for their treatment without sufficient savings.

Living Expenses and Extracurricular Activities: Students need money for personal maintenance, pick-ups, extracurricular activities, and academic needs. Small loans can provide liquidity without burdening the economy with long-term and large debts.

Students Who May Not Have Access to PAN Card

The lack of a PAN card also makes it difficult for many students to use conventional loans. Such challenges often result because financial institutions need documents to confirm a borrower’s identity, income, and creditworthiness. Some of the barriers students grapple with include:

No Real Income and Jobs

Most students depend on their families or work part-time jobs, which do not necessarily generate taxable income. Because students typically do not have a steady source of income, they are often excluded from taking on traditional loans, which require proof of employment and the ability to afford repayments.

No Collateral No Credit History

Lenders consider traditional loans a guarantee of repayment, hence the need for tangible collateral or an excellent credit history. However, students are young borrowers who usually have few assets and no credit history, so lenders will see them as at greater risk.

Documentation Barriers

Most financial institutions have strict documentation requirements for ID, address, and proof of income. In some cases, students may be considered ineligible because a PAN card serves as proof of identity for almost every citizen in the financial system.

Challenging to satisfy the minimum age requirement

Most established loans require the applicant to be at least 18 or 21. Younger students find it difficult to access suitable formal credit options — often due to age-related criteria and the fact they may be financially dependent or work only specific periods in the year.

Alternatives Available

Due to the challenges mentioned above, students whose PAN card is not available or whose income is informal will have limited options for funding their requirements. There are numerous alternatives for permanent students, with quick, small loans or other financial assistance to help them pay their bills.

Scholarships and Grants

Scholars, bursaries, and grants are available for students from academic institutions and private organisations. Financial aid is usually need-based or merit-based and significantly reduces education expenses, including tuition fees.

Scholarships are also a valuable source of unrestricted funding. Still, they should not be relied on as the only source of financial support because they are often competitive, and you may or may not qualify.

Part-time Jobs or Internships

It is open for students to do part-time jobs, freelancing, or internships that they can earn alongside their studies. While earnings from PT jobs are low, they ensure short-term cash influx to cover running bills without taking out loans.

Aid Programs Run By the Government and Institutions

Specific government programs or universities offer students low-interest loans, small stipends, or interest-free loans. These are typically more accessible because they are catered to students, but they might have long turnaround times and/or narrow eligibility terms.

Instant Loan Apps for College Students

Instant loan apps have become the preferred option for students requiring urgent money without guaranteed access to longer-term loans. They usually offer micro-loans with quick disbursal and minimal documentation; they mostly just need an Aadhaar card instead of a PAN.

Most of these are aimed at students, who can pay slowly on small amounts of principal without burdening the bank. As a result, they are appealing to students who require quick money with little to no documentation to qualify for more traditional loans.

Friends and Family Support

Borrowing small amounts from friends or family makes it possible for many students. They are usually interest-free and have soft repayment conditions, which does not mean they function indefinitely.

Formal financial assistance is preferable, but many students cannot access formal aid, or it is insufficient. Instant loan apps help fulfil all your financial needs quickly, and with no need for a PAN card, this is a viable option for many. These apps fill the middle gap for students who need funds to cover academic or emergency expenses but do not have options in a traditional credit setting. However, student loans can come with a hefty price tag — students should be careful about whether they will need to repay their loan and, if repaying is necessary, how much interest will cost them later.

Is a PAN Card Mandatory for a Student Loan?

In India, whether a student loan requires a PAN card will be based on the type of loan, the amount borrowed, and contingent on the lending institution. However, some exceptions exist with student loans or small, instant loans through fintech platforms wherein lenders typically do not need a PAN card as part of the process. Here, we will explain when a PAN card is required, what exemptions students can get, and which documents can be used instead.

Mandatory Requirement of PAN in Loan Application

A PAN card is an essential requirement for the majority of loans in India, but this depends on some details as to when and why a PAN requirement may arise:

Higher Loan Amounts

The financial institutions generally require a PAN card for loans above a specific limit (generally, ₹50,000 to ₹1,00,000 and more) as compliance with KYC and AML.

The PAN card is an official link to the applicant’s tax profile, which helps the lender determine the applicant’s credit risk and financial history. If necessary, the lender can also follow such transactions and report them to tax agencies.

Formal Employment-Based Loans

Individuals in the formal job sector generally request a PAN card. The card serves as proof of income for the borrower; hence, when viewed by any financial institution, it helps them check their tax history and equitable health.

This requirement, particularly regarding high loan amounts for higher studies or professional courses, is more rigorously checked by traditional banks and big financial institutions.

Government-Regulated Loans

For student loans under government schemes like those provided through the Vidya Lakshmi portal, PAN is usually required as a regular KYC paper, mainly if the loan is high-value or security-based.

While PAN might be compulsory for getting government-subsidized loans, private fintech companies and smaller loan apps deviated from the rules.

PAN is used to validate these data and examine creditworthiness in such cases. However, students, mainly those applying for small loans, can get the money without a PAN card based on the lending platform and the amount of loan that they want to apply for.

Unusual Circumstances Regarding Student Loans

Some lending institutions offer more flexible terms, however, which do not require a PAN card and may be suited to students without a comprehensive employment status or taxable income. Many situations and different types of loans give leeway on the documentation process, allowing even young students without a PAN card to avail of this type of financing.

Small, Instant Loan Apps

Most loan apps are targeted towards young borrowers. Their loans are smaller (usually ₹1,000 to ₹50,000) and can be availed easily without a PAN card. These apps are aware of the situation faced by students and try to give money with minimal paperwork.

Instead of a PAN Card ID, they usually ask for an Aadhaar card to establish an Individual’s identity and address proof. This makes the online form much easier to fill out. True Balance, MoneyView, Airtel Loans, and Bajaj Finserv are apps that provide this flexibility for smaller loans.

Lenders with Student-Friendly Policies

Few private lenders have student-specific policies, meaning they may accept the borrower’s Aadhaar card or college ID—and even a document from a guarantor—as proof instead of PAN. Such offerings focused on student saviours can be useful for students applying for short /low-value loans or emergency funds.

Some online lenders also process loans solely based on the student’s Aadhaar details, and income proof or PAN may not be required, benefiting financially dependent students.

Alternative Lending Programs

Relaxed KYC policies are only for students or those with a low credit history. Borrowers: NBFCs (Non-Banking Financial Companies) and digital lenders offer relaxed KYC policies here. The programs were tailored to students who needed immediate cash flow without traditional bank expectations.

Companies like KreditBee and Zype may allow students to apply with minimum ID files, emphasising digital local area network solutions more than the PAN mouth organ.

Alternatives to PAN Card for Student Loans

Students who cannot provide a PAN card will still get a loan against other identity and submission documents. Some widely accepted options are:

Aadhaar Card

Aadhaar card is one of India’s most accepted forms of identity proof. It is a reliable substitute for students without a PAN as it validates identity and address. In particular, Fintech lenders and loan apps readily accept Aadhaar for KYC verification regarding small, unsecured loans.

Student ID

Student Loan Apps: Many student-focused loan apps let people use their college or university ID to verify their student status. This can be especially beneficial when borrowing student-specific loans designated for educational expenses like tuition or classroom materials.

Co-Applicant With Parent Or Guardian

Other lenders let a parent or guardian get stuck with the student loan as a co-borrower. In some instances, the parent’s PAN card and income proof are offered rather than the student’s PAN, thereby avoiding the trouble of obtaining it. A similar structure is prevalent among regular education loans by banks and NBFCs needing collateral or a more significant amount.

Address Proof Documents

KYC may also require voter ID, driving license, or passport documents. These documents cannot be used in place of the PAN for tax-related purposes, but they can help verify the borrower where the case is not strict about providing PAN.

Bank Passbook or Bank Statement

Some lenders may consider a recent bank account statement or passbook for a small loan instead of some KYC documents. This is used to verify the applicant’s financial activity, and it can sometimes substitute a PAN card in specific micro-loan applications.

A PAN card becomes vital for bigger, more formal loans, and there are enough options even if you do not possess one. Students have a panoply of options when securing funds without requiring a PAN card, be it Aadhaar-based loan apps, student ID verifications, or co-applicant setups. These alternatives ensure that students can still access crucial financial assistance, even without formal identification such as a PAN card, thus making financing more inclusive and accessible.

Top Student Loan Apps that Don’t Require a PAN Card

Thanks to the rise of fintech apps catering to students and minor loan seekers, getting a loan without a PAN card has become easier. Now, look at some of the most popular loan apps that do not ask for a PAN card during the entire process. The following are some benefits these apps provide students looking to facilitate easy fund access for school-related and daily expenses.

1. Stucred

Eligibility – Open to Indians; KYC done Online.

Interest Rates: 0% Interest, small service fee applicable

Repayment Duration — 30 days for most short-term loans.

Quick Loan Amount: Upto ₹15000

Flexible KYC: only an Aadhaar card is needed to avail of a small loan; suitable for students. It is the most sought-after quick short-term loan option for students who need money for personal expenses or outside educational needs.

2. MoneyView

Paperless: This option is available for students and unemployed people. They may use their Aadhaar card.

Interest rates: 1.5%-2.5% a month based on credit score

Payments: Flexible payment terms, usually between 3-24 months, depending on which type of loan.

Loan Limit: up to ₹5,00,000, but smaller amounts for students are familiar.

Turnaround Time: Quick turnaround in less than one day.

Borrow as little as ₹10,000 or any amount. This is a fully flexible loan verified through your Aadhaar. It is suitable for students who might need money in emergencies but do not have a conventional banking record.

3. Bajaj Finserv

Features: KYC done via Aadhaar; targeted primarily at salaried people, but may consider smaller loans for students

Interests: Usually from 1.5% to 2.25% per month

Payback Terms: Payback phrases of three to 12 months.

Maximum Loan Amount: ₹1,00,000, but student loans are often smaller

Turn Around Time: If eligible, the funds are disbursed within 1 day

It offers small loans without needing a PAN card to eligible students and individuals. It is ideal for people meeting basic KYC and age conditions due to swift approval time and a big loan limit.

4. Airtel Loans

Who Can Apply: Any person, whether an existing customer of Airtel or not, if they pass the KYC process based on an Aadhaar number.

Interest Rates: From approximately 2% a month, depending on loan type and term

Duration: 62–90 days of short-term loan repayments

Maximum Loan Amount: Upto ₹50,000 for small loans

Fixed interest rates: You will be charged this rate for the life of the loan.

Airtel Loans for Students (through the Airtel app): Airtel also offers loans to students looking for smaller loans. Ultra-fast processing and KYC-based simply on Aadhaar make this loan an easy option for students looking for instant money.

5. Zype

KYC: KYC will be primarily based on Aadhaar and will also focus on customers between 18 and 40, mainly students.

Interest Rates: Approximately 2-3% per month according to the loan amount

Payment Period: Generally short, 30 to 90 days

Small Loans: Up to ₹10,000 only (for small expenses)

Turnaround Time — Loans approved in minutes.

Details: Zype offers micro-loans for students and young professionals who need cash fast. Aadhaar’s unique verification process allows students to use it without a PAN card.

6. Tata Capital

What you need to have: Aadhaar or some form of ID; free policies for students without regular income

Interest: Between 12-15% per year on student loans.

Repayment Terms: Flexible; education-specific loans have longer terms.

Loan Amount: Up to ₹1,00,000 for smaller loans/Maximum amount depending on the purpose of education

Processing Time: Up to 24-48 hours.

Tata Capital is a perfect choice if you need more money for your studies. Known for its lenient eligibility, it is available with Aadhaar verification to students seeking more considerable amounts for tuition and educational expenses.

Key Factors to Consider When Choosing a Loan App

The right loan app will also depend on students weighing the following:

Interest Rates

Interest rates differ significantly, so students must search for apps with the lowest monthly prices to ease repayment.

Loan Tenure

Look at the repayment terms available. The payoff cycle for short-term loans is generally shorter, while student loans might have longer terms designed to cover more considerable education costs.

Simple Steps + Automated KYC

Aadhaar only needs KYC, a boon for students without PAN cards. Use simple application processes for the apps, and less documentation is required.

Quick Disbursal

Many students need money. Instant disbursal time: ideal apps for emergencies and same-day academic needs.

Hidden Fees

Watch for fund handling or late installment expenses. Other charges may contribute to the total cost of borrowing some apps.

This exhaustive list and analysis give students insight into the best loan apps without a PAN card. These signpost points help students weigh their best options for eligibility, interest rates, and ease of access, helping them make the right decision.

How to Apply for a Student Loan without a PAN Card Using Aadhaar and Other Documents

A few fintech apps don’t need PAN and will accept Aadhaar or other documents, so applying for a student loan is possible even without a PAN card. For those seeking fast, versatile financing with no boilerplate documents, here is how to fill out the form top-to-bottom with a few tricks to maximise your odds of sweeping through the loan approval process.

How to Apply: A Step-by-Step Process

Choose the Right Loan App

Look for a loan app that caters to the student segment without requiring a PAN card. True Balance, MoneyView, and Zype are examples of this. Identify apps that support Aadhaar-based online verification.

Download the Loan App

Download the app from the Google Play or App Store. Make sure to download the official app, and beware of fake copies of this body recognition app. Check ratings or reviews to ensure that the one you download is reliable!

Sign up for an account

Open the app and enter your phone number to sign up with — verify it via OTP. You might also be able to sign up using your email with some apps.

Aadhaar and other documents for KYC completion

Fill in the Aadhaar number and complete basic KYC. Other apps may require extra verification, such as taking a selfie and providing your student ID and/or bank/credit card details, to verify that you are indeed who you say you are and have the indicated status.

Input Loan Amount and Payback Term

Select the amount you wish to borrow and pick a tenure for which the refund is comfortable for your budget. Smaller amounts are often suggested for first-time applicants.

Provide Bank Details

Enter your bank account information for payment processing. The above mentioned details must be present, as the funds will be credited to the account by direct loan.

Review the Application and Submit It

Confirm all aspects to avoid delay or rejections. Once you have the registration ready, apply and await approval.

Approval and Disbursement

After approval, the loan amount is typically disbursed in 5 minutes to 24 hours, depending on how fast the app processes your loan.

Where PAN is not Available, What Documents are Required

Without a PAN card, students must submit proof of alternative identity. Below is a sample of the essential documents usually demanded:

Aadhaar Card

It is necessary for KYC (Know Your Customer), including identity and address verification. Keep it updated with accurate information.

Identification Such As A Student ID Or College Enrollment

A college ID or proof of enrollment also works for all student-focused apps and may improve the likelihood of approval.

Aadhaar Linked Phone Number

To make it easier, the phone number attached to Aadhaar must be identical to the one registered on the app. It is essential to get OTP for verification.

Bank Account Details

A bank account in the applicant’s name is required for loan disbursement. Although some apps will accept a digital payment wallet, it’s usually better to the money deposited into a bank account.

Here are some tips for boosting your approval rate:

Aadhaar Linking With Mobile Number and Bank Account

Keep your Aadhaar details linked to your mobile number and bank account. This enables KYC without hassle and can also be verified instantly.

Provide Consistent Information Across Documents

Consistency: You must provide corresponding information about yourself in every document submitted, such as your name, date of birth, address, etc. Differences in the information may lead to verification issues or delays.

Confirm Student Enrollment Status

Sometimes, they ask for student verification a second time within the app. It is helpful to keep your college ID or enrollment letter if further confirmation is required.

Consider Loan Amount and Repayment Terms Carefully

If this is your first application, you should have smaller loan amounts. Paying back your loans on time can help ensure that you can take out bigger loans through the app in the future.

Meet Basic Eligibility Criteria

The majority of applications have minimal age limitations (typically 18+). If you are under 18, apply with a co-applicant.

Maintain a Positive Digital Profile

If the loan app inspects credit scores and online profiles, having a clean record on the net with no overdue accounts can serve as a leg-up.

These guidelines can help students get their loans approved without a PAN card. Every step, from burning a hole in the app of choice to ensuring accuracy in documentation, is crucial for an easy application that rapidly puts money into students’ hands. At the same time, they pay for education and personal expenses

Key Features and Benefits of Using Loan Apps for Students Without a PAN Card

These loan apps that provide financing without a PAN card are aimed at the distinct needs of students. They offer students the flexibility, accessibility, and convenience they need when they might not have the documents to access other loans. Here is a closer look at these applications’ main features and advantages.

Instant Approval

Emergency Disbursement of Funds: The usual loan apps known for quick processing make the funds available to clients within minutes to a few hours of application approval. Fast access is especially advantageous for students who require instant cash for emergencies or unanticipated educational expenses.

Always Open: Instead of having business hours, many apps allow students to apply and receive funds at any time that works best for them.

Flexible Repayment Options

More Flexible Towards Students’ Finances: Most loan apps provide different repayment options to accommodate students who often lack ample income. Terms are flexible and usually last from a few weeks to several months, allowing students to choose a repayment plan that suits their budget.

Interest-free grace periods: Some apps provide a brief, interest-free period for students who may only receive income in intervals (part-time jobs or allowances) by extending due dates to avoid late charges.

Low Amount Home Loans & Small Cash Loans

Loans of ₹1,000-₹10,000: Most student loans are pretty minimal as the loan amount needed by applicants who often need quick loans for daily expenses or emergencies. They are well suited to cover costs like books, stationery, transport, or minor repairs without needing large loans.

Responsible Repayment: The small loans foster prudent borrowing and repayment, allowing students to slowly establish a more positive credit profile without crushing debt.

Digital-Only Process

Completely app-based and No Hard Copy Documents: All loan apps make everything digital only, from application to disbursement. This can be particularly useful for students studying at the other end of the country, who can avoid a trip to the bank or filling in forms on paper inside vessels.

Hassle-free Aadhaar-Based KYC: Apps typically follow Aadhaar-based KYC, simplifying students’ admission without conventional documents. As long as the Aadhaar is linked to the phone number and bank account, all this verification is done within minutes.

Special Student-Centric Benefits

Student-Specific Regular Promotion: Apps have perks just for students, like reduced processing fees or lowered interest rates, to help ease the burden of loans on young borrowers.

Grace Periods and Flexible Terms: Some platforms recognise that students may not always be financially stable and offer grace or interest-free periods, giving students time to spread their repayments.

Loyalty Programs and Cashback Bonuses: Some apps will give loyalty points or cashback for timely repayments, thus rewarding students for doing the right thing!

As a result, loan apps are an ideal solution for students who need financial assistance with minimal hassles and hurdles like traditional loans would require.

Pros and Cons of Using Loan Apps without a PAN Card for Students

Although non-PAN card loan apps provide easy financial solutions for students, consider the pros and cons. A new overview of the advantages and disadvantages of such apps provides a clear guide for students trying to decide whether or not they should borrow.

Advantages

Easy and Convenient Accessibility

Digital-Only Process: These digital loan apps enable students to complete the entire process — from application to disbursement online without visiting a bank.

Low Documentation: Many of these apps will ask for an Aadhaar card, and this low documentation makes it okay for students who do not have traditional documents such as PAN or income proof.

Fast Processing and Issuance

Instant Approval: The loan approves the applications in minutes to a few hours, providing students with quick access to funds during emergencies or urgent academic expenses.

Access: Most loan apps work 24/7, and students can apply for loans and receive funds anytime, even when the bank is closed.

Loan Amounts that are Low and Suited for Students

Designed for Minor Expenditures: These applications provide loans ranging from ₹1,000 to ₹10,000 that can be utilised for day-to-day expenditures such as books, study materials, travel, or other personal expenses so that the pupil cannot bear this enormous debt.

Smaller Repayment Plans: Students will take out less money, which means a shorter period within which they need to repay it. This gives students some comfort with not having a steady source of income as they learn how to control expenses.

Student-Centric Perks

Repayment options: A handful of apps offer flexible repayment terms, like monthly instalments or no-action grace periods, to make it easier for students to accommodate repayments into their finances.

Student Discounts And Rewards: Some apps offer student discounts for processing fees or interest rates and may reward timely repayments with cash back or points, thus making loans marginally cheaper and more rewarding.

Potential Downsides

Higher Interest Rates

Interest Rates From Traditional Loans: These loans are typically more expensive than traditional personal loans, sometimes costing 2-3% a month. This is because documentation is minimal, and there is no credit check.

Total Cost Increase: When interest is added, it can be expensive in the long run because if a student does not repay the debt properly, total costs can increase significantly.

Short Repayment Terms

Short repayment periods: Most student loan apps require repayment within a few months, making it difficult for students without stable earnings. Overly short repayment terms could lead to missed deadlines and damaged credit history.

Strain on Finances: Short terms = students need to plan their money well in advance for the repayments, which may affect them badly if they survive on allowances or part-time work.

Risk of Borrowing Without Income Stability

Risk of Getting into Debt: At this age and without a stable income, students risk getting into debt if they borrow money several times.

Financial Strain: The obligation to repay can create economic pressure, especially if the student is already facing tuition or living expenses.

Hidden Fees and Terms

Processing and Late Payment Charges: A few apps impose processing fees or late payment penalties, significantly inflating the overall expense. These fees are often embedded in the fine print.

Please read Carefully: Students must understand all aspects of whichever loan they apply for. If not adhered to, they can add costly expenses — or even tarnish the credit profile of the student borrower — in the form of hidden fees or terms.

A loan app without a PAN card is easy and available, allowing students to borrow money. However, students must borrow carefully. With this knowledge, students can make more informed decisions to ensure they benefit from the convenience and speed of finding these apps while avoiding any possible pitfalls.

Alternative Loan Options for Students Without PAN Card

However, although these loan apps make it easy for students to get small-ticket loans without a PAN card, they are not the best or cheapest solution. Below are some uncommon loans that students may explore to take a more holistic approach to addressing their financial needs.

Loans Based on Aadhaar Card

Even those without a PAN card take Aadhaar-based loans instead of traditional ones. Such loans use Aadhaar to verify identity and require minimal paperwork.

Coverage and Loan Limits:

The loan amount for Aadhaar-based loans can vary from ₹1,000 to even ₹50,000, depending on the lender’s policies and repayment ability. They can be perfect for short-term costs such as textbooks, transport, or emergencies. Some lenders will offer lower amounts to students.

Benefits:

Minimal Paperwork, Simple Documentation—Because the Aadhaar card is a significant document, qualifying for these advances requires exceptionally short administrative work. Here, an Aadhaar must be present to check identity and bank account points of interest with the appropriate mobile number; in other words, complete data related to people must be assembled.

Quick Processing: Approval and funding are typically much quicker than a traditional bank loan. At the same time, some apps and fintechs have since been disbursing it within hours or almost at the click of a button.

Aadhaar-based loans can reach more people, particularly in rural or semi-urban areas with less prevalent PAN cards.

Risks:

Higher Interest rates—Due to their structure, small loans might be charged higher interest rates than usual, eventually increasing the cost of borrowing.

Strict Repayment Terms: Because the loan amounts are small, these loans usually have short repayment periods, which is less than ideal for students without a stable income stream.

Microfinance Options

MFIs offer small loans to people who are not eligible for traditional bank loans, such as students. They usually focus on empowering disadvantaged sectors and are more lenient about the documentation required of borrowers.

Personalised Assistance for Learners:

For example, there are microfinance lenders who give loans to students without requiring much documentation. These loans are generally low in number and may be meant for specific objectives, such as educational purposes, purchasing equipment, or functional expenses.

Benefits:

Lower Interest Rates: Microfinance loans tend to have lower interest rates than payday loans or cash advances, making them less expensive in the long run.

Adaptable Approval Process: Several MFIs are keen on sanctioning loans to students without steady monthly earnings or PAN cards, as they focus more on other papers such as Aadhaar and educational qualifications.

Risks:

Limited Loan Amounts: Microfinance loans are relatively small, and borrowers have no access to large amounts required for full tuition or significant expenses

Accessibility to MFIs: Access may be constrained in some regions, and students residing in urban areas may find it easier than former area students to avail of these loans through microfinance institutions.

Using College-Based Financial Aid

Students may not be aware of the financial support provided by their educational institutions. Before taking loans, they should always check if scholarships, stipends, and on-campus financial aid programs are available to help finance their education.

Scholarships:

There are often merit-based, need-based, or field-specific scholarships at many colleges and universities. Scholarships are the best financial aid you can receive because they usually do not need to be paid back.

Central Schemes—Many government-supported scholarships and schemes are available for students, particularly during their higher education years. This often depends upon their academic records, family financial background, and occasionally on the community.

Stipends and Grants:

Numerous colleges fund students who work with them in research, teaching, or extracurricular activities through stipends. Students may also receive research grants or assistance in project work at the departmental level.

On-Campus Aid:

Most colleges and universities offer financial aid programs to help with emergency funds or low-interest loans with reasonable repayment terms. These programs are usually tailored to students and offer low interest rates and flexible/forgiving repayment options.

Benefits:

The possibility of not having to repay anything received in scholarships and stipends (scholarships and stipends do not have to be repaid) provides a significant financial break for students.

Designed to help students: These loans are intended for educational purposes, and the eligibility criteria are frequently less stringent than those of a standard loan.

Risks:

Not always available: Only a subset of scholarships and/or stipends are available, so they may not always be available to all students each year.

Wide-Ranging Criteria Related to Earning Potential: Certain financial aid programs have such narrow criteria as to academic performance or categorical status that very few students will qualify, even if they need assistance.

Importance of Planning Repayment for Students

Whether students take a loan through the app or look into other financial options, proper planning and budgeting should be followed to ensure that they do not feel too much pressure and do not end up in a debt trap.

Budgeting for Loan Repayment:

Students should prepare a practical budget with their monthly income, expenses, and what they need to repay. They can save and use those funds to repay their loan, avoiding late fees and interest penalties.

Building Financial Literacy:

Responsible borrowing stems from financial literacy. Students must be aware of interest, how payment schedules work, and what happens if they are late. Several loan apps even provide you with resources and tools that can help you learn more about your financial responsibilities.

Start with Small Loans:

First-time borrowers should take out smaller loans to avoid crushing debt and build a positive credit history.

Conclusion: Simplified Financial Solutions for Students Without a PAN Card

There are no significant roadblocks when availing of student loans in India without a PAN card. Student-specific loan apps offer multiple options with no PAN, only Aadhaar, and other easy documents for fast approval and disbursal. Leading apps for students, in this regard, are True Balance, Bajaj Finserv, MoneyView, Airtel Loans (Airtel app), Zype, and Tata Capital, which all provide quick loans with minimum processing time(low interest rates for student loans) / instant pre-approved loans with borrower-specific repayment terms.

But despite the convenience these loan apps can offer, borrow wisely. Students should thoroughly research each option, comparing interest rates, repayment terms, and other potential fees.” These loans can provide immediate funds to cover tuition and the cost of living, but borrowing more than you can pay back or not planning to pay it back may hurt your financial well-being for a long time.

Pro Tip: Read the loan terms and conditions section carefully before moving to the next step. Keep your loan bad experience free, keep it to the barest minimum and what you can afford to repay quickly. Student loans without PAN cards can be beneficial if appropriately handled to help you fulfil some of your needs as a student and concentrate on your studies.

1. Can I get a student loan without income proof?

Proof of income alternatives for student workers:

That is why students would typically be able to apply for a loan without needing the same type of proof of income. Most lenders understand that students do not have a fixed income. The students can then be asked to submit instead of the income proof:

Student ID: This establishes that the applicant belongs to a learning institution.

Aadhaar Card– Utilized to identify a pupil and link it to their cellular number and checking account.

Income Information of Parent/ Guardian: Students may enter details of a guardian’s income on some apps as an alternative for their income.

This makes credit available to those without formal work or regular income, although it is worth checking with each app to determine what documentation is needed.

2. What’s the maximum amount I can borrow without a PAN?

Standard Loan Amounts for Aadhaar-Based Loans:

The maximum loan amount for student loans without a PAN card depends on the borrowing platform, the borrower’s eligibility, and other documentation submitted — but options are available, typically ranging from ₹1-15 lakhs. Standard loan limits are:

Aadhaar-backed Loans: These are generally ₹1,000 to ₹50,000, although smaller loans (₹1,000 to ₹10,000) are more likely for students. However, many apps provide additional funds based on the student’s credit score or a cosigner’s income.

These loans are only based on Aadhaar, so they are for a lesser amount and used for short-term needs like buying study materials, books, or emergencies.

3. How soon will the funds be disbursed?

Time Taken For Processing the Loans Found on the App:

App-based loans provide quick disbursal time among its many benefits:

For the Loan Apps: Several loan apps offer instant approval and can disperse funds within a few minutes to hours of approval.

Bank Transfer: Once approved, funds are generally transferred directly to the borrower’s linked bank account in about 1 to 3 business days, but this depends on both the lender and the bank.

Ensure all documentation is correct and complete to avoid delays during the application process.

4. Is it legal to borrow without a PAN card?

Clarifying the Legalities:

Yes, it is legal to borrow money without a PAN card. The PAN card is generally required for higher-value loans or loans that involve formal income verification. However, for small loans, especially those using Aadhaar for verification, the PAN card is not mandatory.

Lenders are allowed to use alternate forms of identification, such as the Aadhaar card, to offer loans to students and other individuals without a PAN card. However, it’s important to only borrow from licensed, registered, and reputable lenders to avoid any potential legal issues or fraud.

5. How do I ensure my data privacy on these loan apps?

How to Identify Secure and Trustworthy Apps:

Data privacy and security are crucial for online loan applications. Here are some tips to help you protect your personal information.

Select Verified Apps: Look for applications with good opinions and reputed ratings. Read the app’s privacy policy and make sure it follows good data protection practices (e.g., in-house storage of user/analytical data).

Protected Connections: Confirm that the app connects using HTTPS for encrypted data transfer. Do not use unsecured Wi-Fi networks when applying for loans.

Verify License and Registration: Legal loan apps are typically registered with financial regulatory agencies such as the RBI or a state-run body. They must prominently display their registration details.

Do not Share: Only share the information that needs to be verified. Do not share extra personal details. Provide only essential KYC documents such as Aadhaar, and do not share individual passwords or account details.

6. Which loan app is best for students without a PAN card?

Top Loan Apps for Students:

Following are the top loan apps for student loans without a PAN card:

Proper Balance: True Balance provides micro-loans instantly without a PAN card. This app is famous for fast approval and loan disbursal, with loans ranging from ₹1k to ₹10k. It also helps in issuing Aadhaar-based verification.

Bajaj Finserv: A recognised financial platform that provides instant personal loans for students without a PAN card. You get more excellent repayment terms alongside aggressiveness as a pledge.

Moneyview: For those of you who have heard about instant Personal loan options, MoneyView features loans that can be instantly disbursed with flexible terms without needing a PAN card. Students can also easily benefit from this.

Airtel Loans: Airtel provides instant loans to its customers with minimal documentation, such as Aadhar, which is preferable for students using mobile phones.

Tata Capital and Zype: Both apps provide small loans with Aadhaar verification. They are best suited for students requiring low-interest, short-term loans.