Download StuCred.

The Real Time Student Credit App.

Small Student Loans in India

What Are Small Student Loans?

Small student loans are financial support systems designed to meet the immediate funding needs of students for short-term periods and may range from as low as ₹500 to ₹10,000. These loans can be obtained from multiple financial institutions, such as banks, government schemes, or digital lending platforms. In India, various such loans are available, serving as a boon to students who may need money for different educational activities without incurring large amounts of debt.

The most requested loan amounts are between ₹500 and ₹10,000, which is ideal for students who may not require much but need quick funds for small and urgent educational purposes. Such allowances can involve costs such as acquiring study materials, application or exam fees, and travel for educational visits, among others, which sometimes even extend to reimbursements of living expenses while studying away from home. Student loans are small, which makes them easier to manage, and they are obtained quickly, making them a perfect solution for students who find themselves in a financial crisis.

Importance of Small Loans for Students

It is during times like these that small student loans offer a critical lifeline for students who need immediate funds but are reluctant to take on large, longer-term debts. These loans are frequently processed rapidly, with minimal paperwork — a fitting option for students who need the flexibility to cover unexpected expenses. They can help students afford to buy books or pay small fees, and the loans are available to ensure that their education doesn’t suffer due to financial-related costs.

Apart from traditional banks, digital lending platforms such as StuCred and InstaPocketLoan have changed the way people avail themselves of small loans. These platforms offer fast, easy, and hassle-free loan disbursements, requiring no collateral, making them easily accessible to students who may not have access to the financial means typically required by banks.

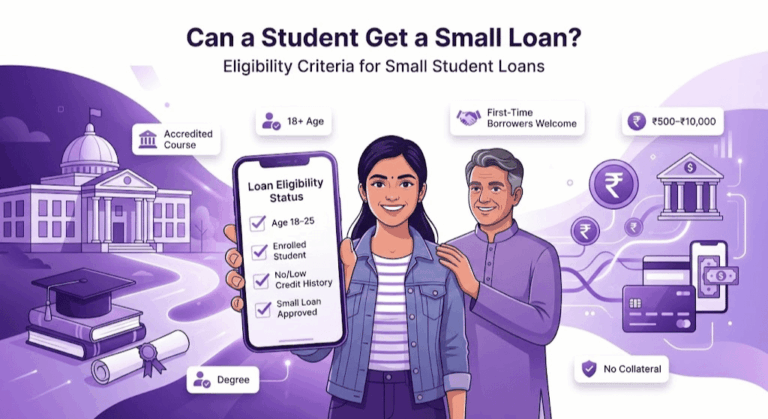

Can a Student Get a Small Loan?

Eligibility Criteria for Small Student Loans

Eligibility for small student loans in India includes age, education status, and financial history. Most lenders, including major banks such as Tata Capital, HDFC, and Bank of Baroda, have general eligibility criteria for students to apply for small loans.

Age: Most applicants should be between 18 and 25 years of age. Some lenders may offer loans to younger students, especially when the student is pursuing a post-secondary education or has established a financial history.

Education: Students must be studying at an accredited university, pursuing undergraduate, postgraduate, or vocational courses. Some lenders also offer loans to take online classes or pursue other certifications. HDFC student loans, for instance, require documentation confirming enrollment in an accredited program.

Financial history: Since many small loans are unsecured (i.e., without collateral), lenders may review the applicant’s credit history, including whether the student has an existing relationship with the bank. However, first-time borrowers are not required to have a lengthy credit history, as long as they meet other basic eligibility requirements.

Here’s how each lender works:

Tata Capital: It offers loans with minimal documentation and prefers students with a clear academic history.

HDFC offers loans to students for overseas and higher education, and can even provide loans to students with no credit history.

Bank of Baroda: The course of study and future repayment capacity of the student, as well as their financial background, are taken into consideration.

Loan Types for Students – Small Student Loans

Students are left with either a personal loan or an education loan when it comes to a small student loan.

Personal Loans: These are unsecured loans that can be used for any purpose, including educational finance. Each bank has its eligibility requirements, which broadly include an income, credit score, and relationship with the bank. Personal loans generally carry higher interest rates than education loans, and their repayment terms may not be as flexible.

Education Loans: These are loans provided explicitly for educational purposes. They can have lower interest rates, more extended repayment periods, and deferred repayments while the student is still in school. These loans typically demand proof of a student enrolled in an accredited institution.

When availing of these loans, banks and non-banking financial companies (NBFCs) check a few things:

Credit Score and Financial Standing: The credit score of the applicant is what lenders primarily look for when considering personal loans. However, for education loans, this is not usually applicable to first-time borrowers, especially those below ₹ 10,000.

Course of Study: Lenders prefer students who are enrolled in classes with good job prospects, as this increases the likelihood of loan repayment by the student.

Post-Graduation Repayment Ability: Lenders assess whether the student will be able to repay the loan after graduation. This will depend on the course the student chose, their job prospects, and whether they have any part-time income.

Student Loan Eligibility for First-Time Borrowers – Small Student Loans

Whether an 18-year-old student can apply for a loan is one such question. Yes, but, of course, they must meet the basic eligibility requirements, i.e., complete an approved course of study. Students are considered legal adults at 18, meaning they can apply for loans in their name, but may need a co-applicant (often a parent or guardian) to strengthen their application.

Many banks and digital lenders are willing to provide small loans to first-time borrowers, even if you lack a credit history. Some factors that can help increase eligibility for first-time borrowers are:

Good background (or enrolled in a high-demand course (engineering, medicine, or business studies).

A co-borrower with strong credit or steady income.

Collateral: Many loans are for small amounts and thus no collateral is needed; however, larger education loans will require a guarantor or collateral. However, some of these digital platforms offer unsecured loans with small amounts (such as ₹5,000 to ₹10,000) without collateral.

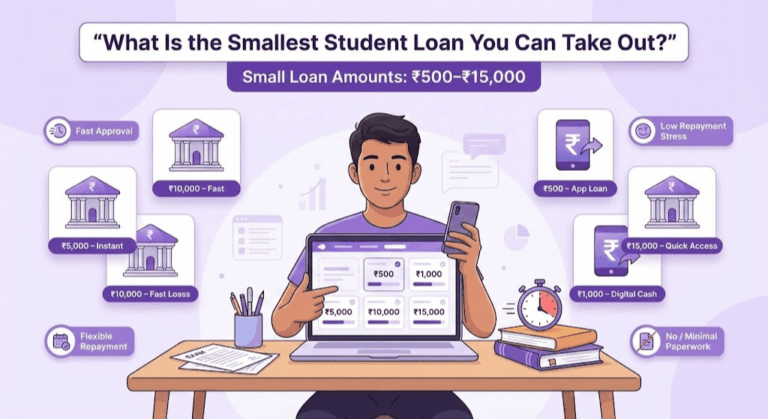

What Is the Smallest Student Loan You Can Take Out?

Small Loan Amounts Offered by Different Lenders

In India, some lenders offer small student loans to address short-term educational needs (immediate costs associated with school or college) or personal needs. The minimum student loans generally vary between ₹500 and ₹10,000, depending on the lender as well as the type of loan.

Tata Capital provides education loans in smaller sums, for students to cover immediate educational needs – whether that be buying books or paying application fees. These are low dollar amounts and can be tailored to specific student needs, making them flexible for small-scale expenses.

HDFC offers loans for educational purposes, covering tuition fees, study materials, and other essential student needs. The loan amount is flexible according to the student’s needs and the course they are pursuing.

Bank of Baroda offers small loans with easy processing for students who need to raise urgent funds. They are designed to assist students with smaller costs and typically do not require collateral or a co-applicant.

Besides these fixed loan amounts, many digital lending platforms, such as StuCred and InstaPocketLoan, offer flexible loan amounts, students can borrow as low as ₹500 and as high as ₹15,000. That makes these platforms attractive, as they usually provide speedy disbursement times and minimal paperwork.

What Makes Small Student Loans Attractive?

For students, dealing with small loan amounts brings less stress and more freedom:

Faster Approval: Since the loan amounts are small, the approval process is significantly quicker compared to larger loans. Most lenders, particularly digital lending platforms, offer instant loans with approval within minutes.

Lower Repayment Pressure: Since smaller loans result in smaller monthly repayment amounts, making them easier for students to handle. This is particularly true for students who may not have a consistent source of income and require immediate financial assistance.

Flexible Repayment: Some lenders break down repayment of microloans into smaller installments, making budgeting simple. To make things easier, some banks and NBFCs also provide deferred repayment options, which means that you need to start repaying the loan only after completing your education and securing a job.

To begin with, government-insured loans tend to have lower interest rates than those offered by private lenders. Most government education loans have an interest rate of 7% to 9% for courses that the government subsidizes. Private lenders, such as Tata Capital and HDFC, on the other hand, typically charge slightly higher interest rates — ranging from 10% to 15% — depending on the loan amount and term. However, private loans are a popular immediate option — they require less documentation, and the processing is much faster.

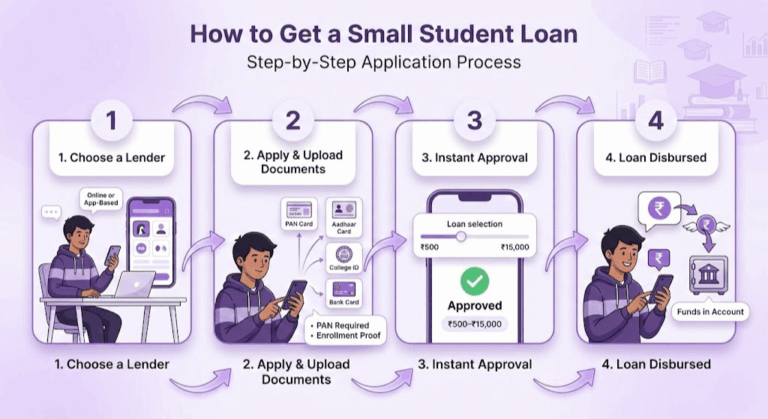

How to Get a Small Student Loan?

Step-by-Step Process for Applying

Applying for a small student loan is a relatively simple process if you know what you need to do to ensure your application is complete and accurate. Here’s a step-by-step guide on how students can apply for loans with the different institutions.

1. Research and Choose a Lender: The first step is to research lenders that offer small student loans. Some of them include HDFC, Tata Capital, and Bank of Baroda. Shop around for the terms, interest rates, and loan amounts that meet your needs.

2. Fill out the Loan Application: After selecting your lender of choice, the next step is to complete the loan application. This will also ask you for some basic personal information, such as your education (institution, course, etc.) and financial status.

3. Should ensure the required documentation is provided:

Acceptance/Enrollment Confirmation: Applicants must provide proof of acceptance or enrollment at an accredited post-secondary school. This could be a college ID, admission letter, or fee receipt.

PAN Card: A valid PAN card is mandatory when applying for a loan to identify you.

Bank Account Details: Lenders will request the bank account details to credit the loan amount directly.

Identity Proof: In addition to a PAN card, you may also be required to provide an Aadhaar card or voter ID as identity confirmation.

Co-applicant Information (if Applicable): Some lenders may require a co-applicant (typically a parent or guardian) as a guarantor for the loan, especially if the applicant has no previous credit history.

4. Submit the Application and Documentation: Submit your completed application form and relevant documents either online or at the lender’s branch. Many digital platforms and banks allow students to do this via their websites or mobile apps.

Taking a Loan digitally through online lending platforms

Digital lending platforms, such as StuCred, InstaPocketLoan, and Cashe, have revolutionized the way students apply for small loans. These platforms enable instant approval, require minimal paperwork, and offer quick disbursement times. Here’s how to apply:

Step 1: Download the App: Download the app of your preferred lending platform. To illustrate, StuCred is an app accessible on iOS and Android.

Step 2: Register on the app using your phone number and email, and complete your details. You will need to upload documents such as your PAN card, proof of enrollment, and identity verification.

Step 3: Choose Your Loan Amount: Depending on the platform’s limits, ranging from ₹500 to ₹15,000, select your required loan amount. These platforms verify your details and enable you to adjust the loan limit according to your needs.

Step 4: Quick Approval: Digital platforms often have approval processes that can be instant in some cases. After you submit the documents, the platform typically processes the application within a few minutes. Obtaining a quick and simple decision through the automated approval process is not done by people; it is based on algorithms.

Loan Disbursement: Once approved, the loan amount is typically disbursed directly into your bank account. The process is relatively quick compared to traditional banks, where disbursement can take up to 24–48 hours or even occur within minutes in some cases.

Loan Approval and Disbursement

Small student loans are generally quick to approve and disburse, compared to larger loans. Here’s what students can look forward to:

Waiting Time for Approval: For HDFC, Bank of Baroda, and other traditional banks, approval time can take anywhere between 3 and 7 working days. The timing may vary based on the loan size, the documentation required, and the lender’s internal processing timelines.

Instant Approval: On digital platforms such as StuCred and InstaPocketLoan, loans are approved in minutes. This means that there is little paperwork, and approval for a student loan can happen faster through these platforms, which is excellent for students in dire need of funds.

Disbursement Duration: Traditional banks take approximately 3-5 days to disburse the loan amount, whereas the digital platforms transfer the amount to the bank account within 24 hours.

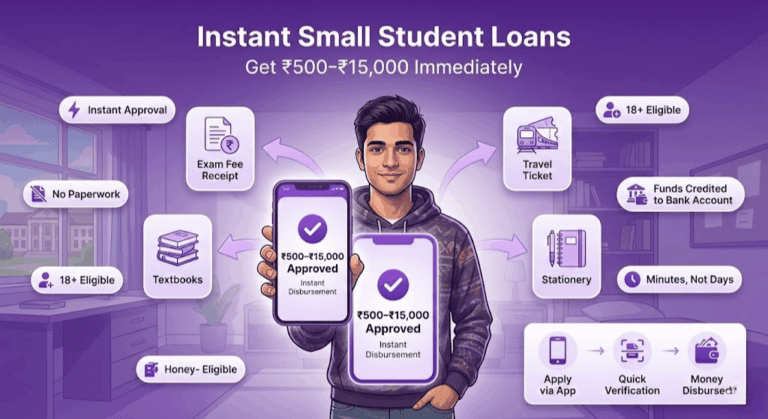

Instant Small Student Loans for Students

How to Get ₹500 to ₹15,000 Immediately

For emergencies, students sometimes require quick access to small loans to pay a fee, purchase study materials, or cover an unexpected expense. Luckily, a few digital lending platforms and banks offer instant loans of ₹500-₹15,000 with instant approval and disbursement.

StuCred: One of the leading digital lending apps, provides instant loans ranging from ₹500 to ₹15,000. Loans are approved through the app, enabling students to receive access within 24-48 hours, often in as little as 15 minutes after approval. The application process is fast and requires little documentation.

Tata Capital: Tata Capital offers a simple Instant Personal Loan feature, through which students can take a loan of ₹5,000 to ₹10,000 in minimal time. The loan also provides quick access to funds, being disbursed within 24 hours, which is highly beneficial for students in immediate need of funds.

To qualify for an instant loan, students typically download the lender’s app or visit the official website, where they can fill out a loan application along with their basic personal details, such as their PAN card and proof of enrollment. After a course of study has been approved, the funds are transferred directly to the student’s bank account.

Eligibility for Instant Loans

Students must satisfy the eligibility requirements to apply for instant loans. While requirements vary from platform to platform, a few general rules of thumb are:

Minimum Age: Most digital platforms and banks require applicants to be at least 18 years of age to apply for an instant loan. However, students under 18 can use it if they have a co-applicant, typically a parent or guardian.

Credit Score: Instant loans are usually catered toward first-time borrowers, but a good credit score can still boost your likelihood of approval. Some platforms, such as StuCred, may provide loans even if an existing credit score is not available and use alternatives, including financial behavior and educational status.

Required Documents: Students generally need to submit:

Identity Proof (PAN card, Aadhar card, etc.)

Proof of Enrollment in a recognized educational institution (e.g., college ID, admission letter)

Bank Account Details for Disbursement

Income or Financial Support Proof (for co-applicants, if any)

Advantages of Instant Loans for Students

Given their speed and convenience, instant loans appeal to students who require immediate access to money in this situation. The following are the top benefits of choosing an instant loan:

Rapid Approval: On-the-spot approval and disbursement within hours enable students to access funds without delay. This is especially useful in cases where students encounter emergencies or unplanned educational expenses.

No Paperwork: Most digital lending platforms do not require detailed documentation, making the loan application process frictionless. This is in contrast to traditional loans, which can require extensive verification and paperwork.

Immediate Access to Funds: Students can instantly use their loan funds to purchase textbooks, fill out application forms, and pay for travel expenses for exams as soon as they are disbursed. Timely access to these funds can alleviate financial stress and enable students to focus on their coursework.

Overall, instant loans are a convenient solution for students in urgent need of financial assistance, as they require minimal documentation and provide quick access to funds. Using platforms such as StuCred, Tata Capital, and Bank of Baroda, students can obtain loans ranging from ₹500 to ₹15,000 almost instantly.

Personal Loan for Students (Small Student Loans) vs. Education Loan

What Is the Difference Between Personal Loans and Education Loans?

When it comes to financial aid for students, the two most common types of loans are personal loans and education loans. They both serve different purposes and have distinct features. Now, let’s examine what differentiates these loans.

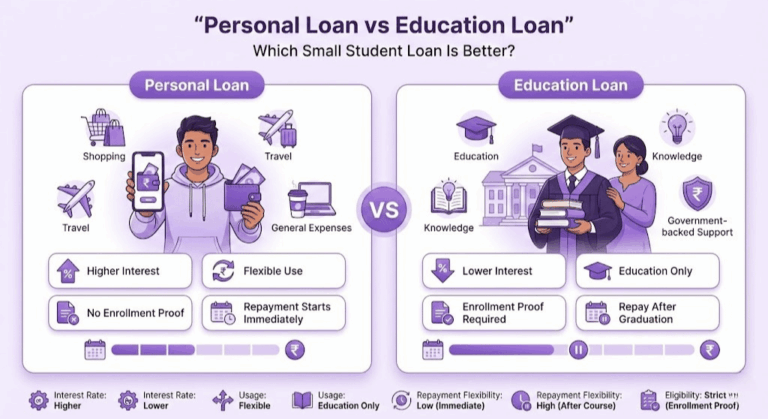

1. Why a Personal Loan for Students: A personal loan for students is an unsecured loan that can be used for a variety of expenses, including tuition fees, book purchases, or other miscellaneous educational costs. Personal loans require no proof of enrollment or academic documentation, unlike education loans. These loans are typically unsecured, meaning they don’t require collateral, but they may come with higher interest rates than education loans.

Essential Features of Personal Loans:

However, you don’t have to use it just for educational expenses.

Usually comes with a higher interest rate than education loans.

In general, it does not require academic enrollment proof.

Repayment terms: Flexible, commonly between 1 and 5 years

2. Education Loan: As the name suggests, an education loan is intended for students who require financial assistance for their education. These will cover tuition fees, books, stationery, travel expenses, and even living expenses while studying. Typically, education loans require proof of enrollment in an accredited educational institution and are usually secured by government schemes, which make them cheaper in terms of interest rates.

Main Features of Education Loans:

Designed only for educational expenses.

It may require proof of enrollment at an eligible school.

Low interest rates, especially for government-backed loans.

The loan repayment begins after course completion, giving students a grace period.

Can require collateral or a joint applicant (often a parent or guardian).

Which Loan Is Better for Students?

The decision to opt for a personal loan or an education loan often comes down to the purpose of the loan, as well as the student’s requirements and eligibility. Let’s compare both options based on key factors:

Purpose of Loan:

Education Loan: If the loan is specifically intended for academic purposes, such as tuition fees, study materials, or overseas education expenses, an education loan would be a better choice. It also features lower interest rates and a flexible repayment plan after graduation.

Personal Loan: If your needs are not limited to education, and you may be looking for funds for other expenses as well (such as living, travel, etc.), a personal loan is more flexible. While it can be used for a wide range of expenses, it tends to have a higher interest rate and more stringent payment requirements.

Interest Rates:

Education Loans: Interest rates tend to be lower, particularly with government-assisted loans. This means it can be a great deal for borrowers who require significant assistance with paying for their education.

Personal Loan: Personal loans are unsecured loans; therefore, their interest rates are generally higher. That means students can pay significantly more in interest on an education loan over time.

Repayment Flexibility:

Education Loan: Education loans are one of the few types of loans that come with a grace period, which means you can start repaying the loan once you have completed your education or secured a job. This provides students with financial security as they embark on their careers.

Personal Loan: You typically begin paying back a personal loan immediately or within a short time, and the terms are stricter. Almost immediately, students are required to start paying interest on the loan, which can be detrimental if they are not financially sound.

Loan Amount and Eligibility:

Educational loans: Education loans are in high demand, as most students opt for overseas education for better opportunities, thus they offer higher loan limits. However, if the loan amount exceeds a particular level, they may require a co-applicant or collateral.

Personal Loan: The loan amount for personal loans is relatively lower than that of education loans, and they may have unaffordable eligibility criteria, especially for students who lack a credit history or have no co-applicant.

Conclusion

With a personal loan, an individual receives a lump sum of money from a lender and pays interest on it. However, for educational expenses, education loans are a preferable option because they offer a lower interest rate and flexible repayment options. By contrast, personal loans offer more flexibility in their use, but they typically come with higher interest rates and more stringent repayment schedules.

Small Loan Options Without Collateral – Small Student Loans

Unsecured Loans for Students

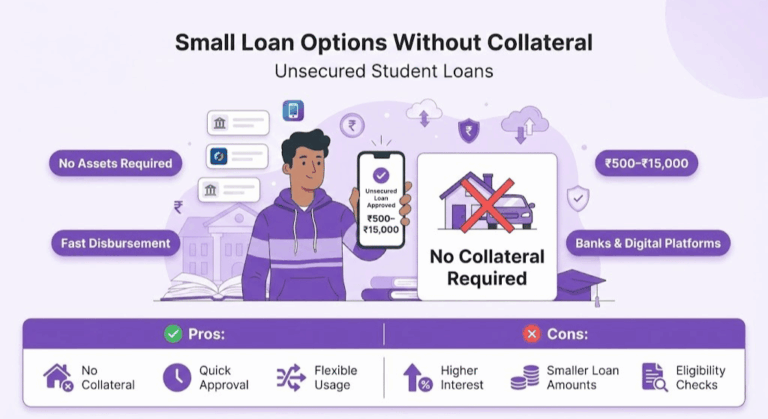

If you are a student seeking quick access to cash without requiring collateral, unsecured loans are a great option. The appeal of unsecured loans is that no assets (such as a house or car) are pledged against the borrowed money, which may be an attractive option for people with assets. Various lenders, including traditional banks, non-banking financial companies (NBFCs), and even digital platforms, offer small student loans without requiring collateral.

The best lenders for unsecured loans include:

Tata Capital: Tata Capital is also a popular lender when it comes to offering student loans without requiring collateral. These loans help cover expenses such as tuition, study materials, and other educational fees.

HDFC Bank: HDFC personal loans for students are unsecured personal loans that do not require any collateral. HDFC offers a wide range of loan amounts for students, from ₹30,000 to ₹15 lakh, making it another popular choice for students planning their higher education.

StuCred: StuCred is a digital lender that provides instant unsecured loans from ₹500 to ₹15,000. It’s an excellent option for students who need less money for essentials like books, travel, or fees right now.

Bank of Baroda: The Bank of Baroda is associated with education loans. Still, they also offer personal loans for students without requiring collateral, making it flexible for students to find a loan option that suits their requirements.

Pros and Cons of Unsecured Loans

Unsecured loans provide easy access to funds without the need for collateral; however, they do come with some trade-offs. In this article, we examine the advantages and disadvantages of choosing an unsecured loan for your education.

Pros:

No Need for Collateral: The primary benefit of unsecured loans is that these are not secured against any asset. These loans can be applied for by students without significant assets.

Faster Disbursement: There is no need for the verification of the collateral, as a result, the unsecured loans are processed more quickly than secured loans. This is especially useful when students require funds rapidly.

Flexibility in Fund Use: Unsecured loans can typically be spent on anything — educational or personal. This allows students to use the loan amount for tuition fees, books, living expenses, or any other study-related need.

Cons:

Higher Interest Rates: Unsecured loans carry a higher risk for lenders, so they are typically more expensive than secured loans in terms of interest rates. That means students could end up paying more in interest over the life of the loan.

Smaller Loan Amounts: Unsecured loans typically have lower loan limits than secured loans. In case a student is expected to lend a huge chunk (let’ss say ₹10 lakhs for studying overseas), they might not be allowed to borrow that amount without collateral.

Stringent Eligibility: No collateral is required, but there is a wide range of factors, such as a good credit score, proof of income, and a stable financial history, that the lender may look for before approving the loan.

Eligibility and Documentation

Although unsecured loans do not require collateral, lenders do have eligibility and documentation conditions that must be met. The key elements that provide insight into whether a student qualifies for an unsecured loan are as follows:

Age and Educational Status: Generally, lenders require pupils to be at least 18 years old. Students should enroll in an accredited educational body, irrespective of whether it is a college, a university , or a professional course.

Credit Score: You need to have a good credit score to qualify for an unsecured loan. Lenders use credit scores when evaluating a borrower’s ability to pay back the loan. So, to get your approval for a bank loan on digital platforms without a credit score is not going to be possible, as traditional banks, for example, HDFC, Tata Capital, need you to at least have some minimum score (650-700 generally).

Income Proof (Co-Applicant): Most students need to apply for a loan through a co-applicant (like a parent or guardian). Proof of the co-applicant’s income, such as salary slips or bank statements, will be required to verify the borrower’s financial stability.

Documentation:

Proof of Address: Aadhar card, utility bill

Annual Confirmation Note from Institution in use (Maintaining Letter, School ID)

Bank Statement (of co-applicant or personal account)

Conclusion

For those who require swift financial support without collateral, unsecured loans for students are the ideal solution. They offer a versatile method to finance both educational and personal expenditures, particularly in situations where different types of loans may demand a considerable amount of documentation or the collateralization of valuable property. However, students should be mindful of higher interest rates and stricter eligibility requirements. Awareness of the advantages and disadvantages, as well as the documentation required for sanctioning aids , helps students make an informed decision when applying for these loans.

Loan Application Process and Tips – Small Student Loans

How to Maximize Your Chances of Approval

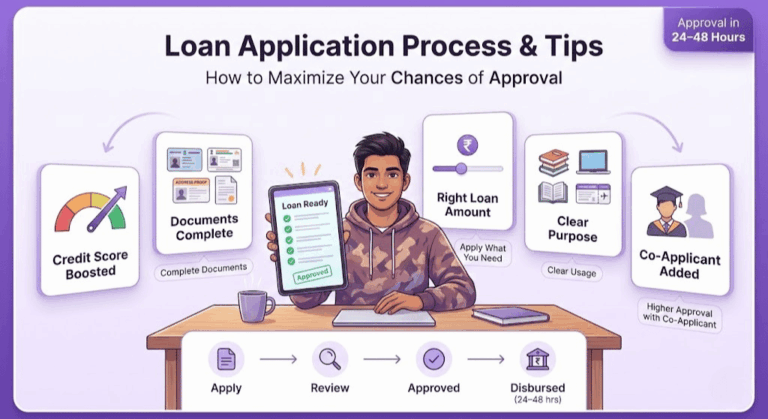

Obtaining a small student loan is not just a matter of filling out an application form. Here are a few steps you can take well in advance of your application to improve your chances of getting approved:

Maintain a High Credit Score: A high credit score is one of the primary factors lenders consider when determining loan approval. Your credit history matters even when you’re borrowing on unsecured terms. Having a co-applicant with a strong credit score can increase your chances if you’re a first-time borrower.

Submit all required documents correctly: Ensure that you submit all the necessary documentation. This typically includes:

Proof of Identity (Aadhar card, PAN card)

Proof of Address (Utility bill, Aadhar card)

Admission letter (University enrollment proof) or student ID

Proof of Income (For co-applicant, if applicable). Missing or incorrect documents can delay the approval process or lead to rejection.

Apply for the Right Amount of Loan: It’s always tempting to borrow more, but apply for the loan amount that you actually need. Applying for loans that are too large for what you want to achieve may deter lenders.

Make Your Purpose Very Clear: Lenders like to see if the borrower’s purpose is clear. If you’re using a portion of the loan for tuition fees, study materials, or living expenses, being transparent about how the loan will be spent can help.

Find a Co-Applicant: Since your credit history is limited, consider adding a co-applicant, typically a parent or guardian, to your loan application. The financial stability of the co-applicant reassures the lender.

Loan Processing Times and Approval Rates

How long does it take to process a loan? Generally speaking, here is what you can expect:

Processing Times: Traditional banks (HDFC, Tata Capital, Bank of Baroda, etc.) However, in the case of digital lending platforms such as StuCred or InstaPocketLoan, the process takes a significantly shorter time. If you have your documentation and eligibility in place, you can expect loan approval and disbursement within 24 to 48 hours.

Approval Ranking: The approval rates may vary depending on several factors, such as the number of applicants applying directly and their credit score, income, and loan amount. Banks, especially when it comes to unsecured loans, often have stricter approval criteria. While approval for small loans may be easier with digital lenders, the interest rates are higher.

The approval criteria are relatively less strict as compared to banks that typically require a co-signer with a stable income, hence, digital lenders such as the StuCred or the InstaPocketLoan can be an option for most students who need a small amount to be disbursed quickly.

Conclusion – Small Student Loans

Various small student loan options are available to students in India. There are many options if you want a small loan to pay for study materials, college fees, or for immediate needs. From traditional education loans provided by banks like HDFC, Tata Capital, and Bank of Baroda to digital lending platforms like StuCred and InstaPocketLoan, students can obtain instant loans ranging from ₹500 to ₹15,000 or more. Students need to consider what type of loan best suits their needs, its eligibility criteria, and how much they would need to borrow for their education (personal loans, education loans, or unsecured loans).

Final Thoughts

Students should also compare loan terms, interest rates, and repayment schedules before applying for any loan. It’s crucial to select a loan that aligns with your financial situation and academic goals. The details surrounding small student loans and government-backed education loans may seem overwhelming, but the more you understand about grants and loans, the more successful your financial application will be.