Download StuCred.

The Real Time Student Credit App.

Student Loans for College Students in India — Complete Guide

Understanding Student Loans in India: Basics and Who Should Apply

What is a student loan? (definition and key features)

A student loan (or education loan) is a form of debt used to finance tuition and living expenses incurred during higher education. They include a fixed loan amount, an interest rate, a repayment period, a moratorium (study + grace period), documentation, and, usually, a co-applicant. Loans may be secured (with collateral) or unsecured, and many lenders permit partial disbursements directly to the institution.

Student loan types in India (education, skill development, vocational and international studies)

Domestic Higher Education Loans: Tuition Fee, Hostel fee, and all books & project costs for Indian universities and colleges (UG/PG/PhD)

Skill development and vocational loans: Short-term courses, certificate programmes and skill upskilling which banks/NBFCs offer with specific eligibility criteria and generally small loan sizes.

International education loans: Typically for studying abroad, covering tuition, living expenses, airfare, and, at times, pre-departure costs; higher collateral requirements and additional documents needed.

Specialized loans: MBBS / medical abroad loans, and professional courses (management, engineering); distance education/sponsored research.

Alternatives to loans: develop alternative repayment structures, such as NBFC-sponsored products under a somewhat new income-share agreement (ISA) model:

Who should consider a student loan? (financial profiles, alternatives)

Consider a loan if:

- There is not enough family savings, and there are only scholarships to cover a little bit of school and only the basics for living.

- Borrowing is worthwhile due to the potential returns (job opportunities, income growth).

- You have a co-applicant with good credit (usually a parent) and a definite repayment plan.

Alternatives:

- Scholarships, grants, and fee discounts.

- Part-time work, internships, assistantships, and campus jobs

- Corporate sponsorships or education crowdfunding

- Any personal savings or contributions from family members.

- Loans are especially suitable for low-income households who qualify for interest subsidy schemes.

Key terms explained (principal, interest rate, moratorium, EMI, collateral, co-applicant)

Principal: The amount of loan issued out or how much you are borrowing.

Interest rate: what it costs you to borrow the money, per annum.

Moratorium: A period during which repayment is deferred (often course duration + 6–12 months); interest may or may not accrue depending on the scheme.

Equated Monthly Installment (EMI): The regular monthly compensation of the principal and interest.

Collateral: This is (property, FDs) the asset pledged to secure the instant 20 lakh loan; usually needed for bigger loans.

Co-applicant: Usually a parent/guardian with joint income; their income is used for qualification.

Student loans vs. scholarships and education grants

Repayment: Loans are paid back with interest; scholarships and grants do not have to be repaid.

Eligibility: Scholarships are either merit- or need-based, while loans are based on your credit. Documentation of income is required.

Cash flow impact: Loans provide cash flow and create long-term liabilities, whereas scholarships reduce or avoid debt.

Complementary use: Scholarships may reduce loan size; a combination often optimizes costs.

Who should avoid student loans?

- If expected salary uplift is uncertain (high-risk courses with poor placement statistics)

- If cheaper options (full scholarships, family supplementation) are in play.

- If the co-applicant has bad credit or the family cannot bear the repayment stress.

Quick decision checklist

Verify course ROI and placement historical past.

Look for scholarships or institutional aid

Shop the lenders for rates, fees & moratorium terms.

Create a repayment strategy—build EMIs based on post-graduation income expectations.

Read more

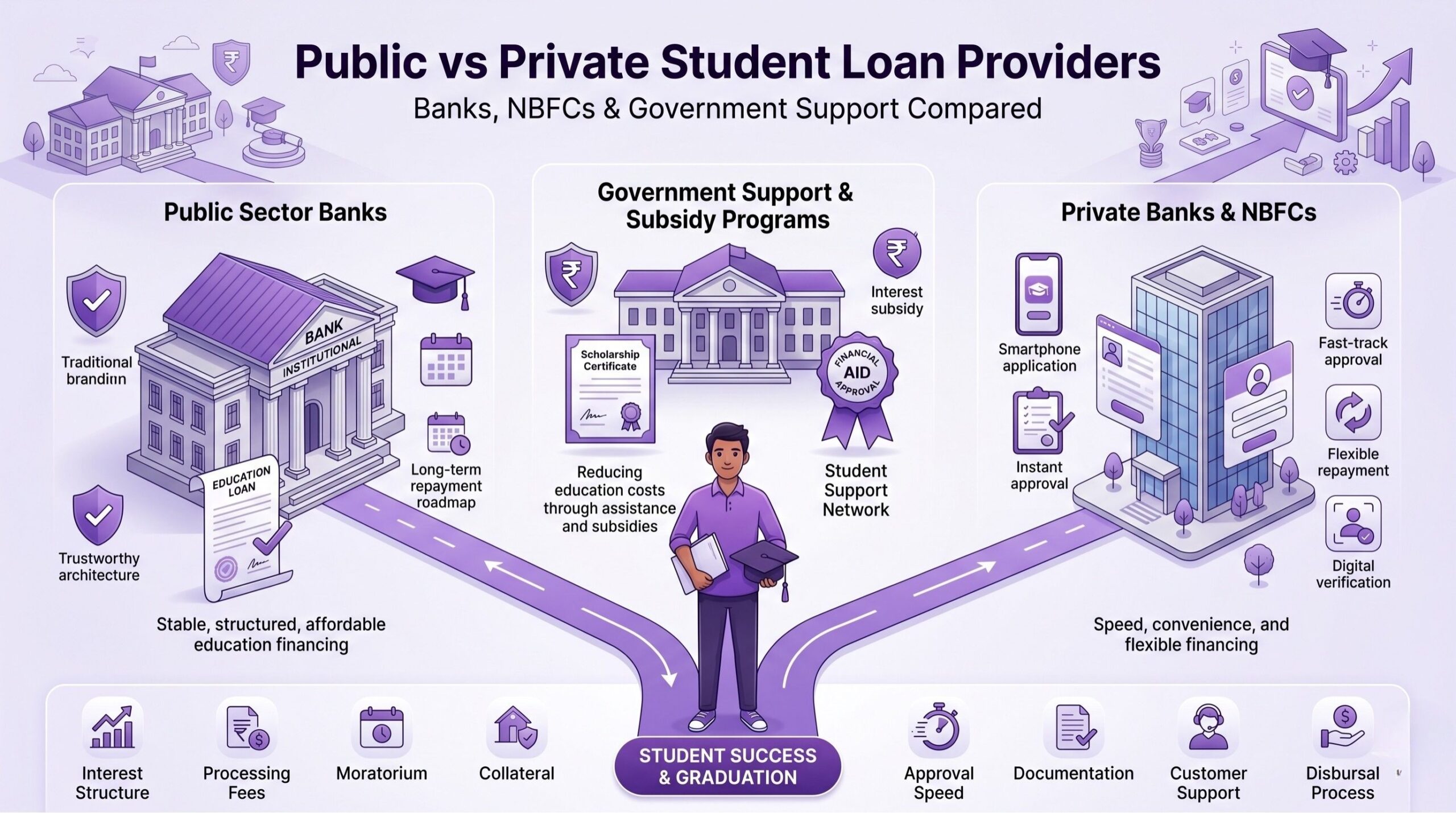

Public vs Private Lenders: Banks, NBFCs, and Government Schemes

Major public sector banks and their flagship student loan products (SBI, PNB, BoB — what to expect)

Low interest rates, vast branch networks and established processes keep education loans popular in public sector banks.

The State Bank of India (SBI) is one of the largest education loan providers, offering flexible tenures, moratorium options, and tie-ups with institutions. SBI offers special schemes for meritorious students, government-sponsored courses, and rates pegged to the MCLR/external benchmark.

Punjab National Bank (PNB): One of the best education loan providers, offering a full range of domestic and international education loan products, PNB also provides affordable margins and simple documentation for children of PSU employees.

Bank of Baroda (BoB): Education loans up to large ticket sizes, especially for reputed institutions, and other lower margins sometimes applicable as well for government-recognised universities.

Expectations with public banks:

- Competitive interest rates (could be marginally less than NBFCs for secured loans)

- Delay at the front end in some branches but effective grievance redressal.

- Uniform documentation and open fee structure

Private Banks and NBFCs (HDFC, ICICI, IDFC, Credenc and Avanse — features & flexibility)

Private lenders & NBFCs have made inroads with product innovation and quicker approvals.

HDFC Bank and ICICI Bank: Customised loan packages, flexible repayment options (step-up/stepdown EMIs), fast digital processing, with marketing tie-ups with leading colleges

IDFC First Bank: Competitive rates, digital onboarding; but emphasis on salaried co-applicants

Avanse and Credenc (non-banking financial institutions, or NBFCs): Focus on education finance with customised products for students, higher unsecured instrument limits for identified borrowers, easy process & counselling service. NBFCs offer more types of collateral, and disbursal is much faster, too.

Advantages of private lenders/NBFCs:

Quicker turnarounds, more digital processes and a readier disposition towards financing international research or country-specific programs.

Attractive repayment structures and an orientation towards customer service.

Trade-offs:

A little more interest or processing charges than public banks, more so for an unsecured loan.

List of Government schemes and interest subsidy (Central Scholarship/PG Scholarship, Central Sector Interest Subsidy (CSIS) for PG, Vidya Lakshmi portal)

Vidya Lakshmi portal: A centralised government portal to apply for all education loans and scholarships; Built-in facility to read the status of multiple loan applications.

Central Sector Interest Subsidy (CSIS): Full-time professional/technical courses are eligible for the scheme; the government pays interest during the moratorium period for eligible categories, thereby reducing costs.

Central and State Scholarship Portals: It is a form of direct financial aid that makes you less dependent on loans

Prime Minister and state efforts are practised from time to time for financially weaker students or specific disciplines.

Tie-ups and campus finance options for educational institutions

From on-campus loan counselling to priority processing and special loan products, numerous colleges and universities partner with banks and NBFCs. The financing used by many campuses makes documentation and disbursal easier, sometimes even providing negotiated fee schedules or partial funding.

How to Compare Lenders: Fees, Margins, Time/Processing Docs

- Structure of interest: Fixed v/s floating, base rate (MCLR) or External Benchmark + Spread

- Spread & margins: The margin that a lender adds to the benchmark.

- Processing Fees and GST: Initial cost to disburse the loan.

- Prepayment/foreclosure charges: Fees related to early repayment

- Collateral requirement & valuation rules

- Moratorium conditions and plans for whether interest accrues during it.

- Loan disbursal: Directly deposited into the institute or with the borrower, staged transfers

- The time taken to sanction and disburse.

Grievance redressal, branch reach, customer service

Understanding which lender to select will depend on the nature of the course, the loan amount, and whether you have or need collateral. Public banks could be cheaper for domestic loans over the long term; however, if you are looking for international studies or faster processing, NBFCs or non-public banks might come to your rescue.

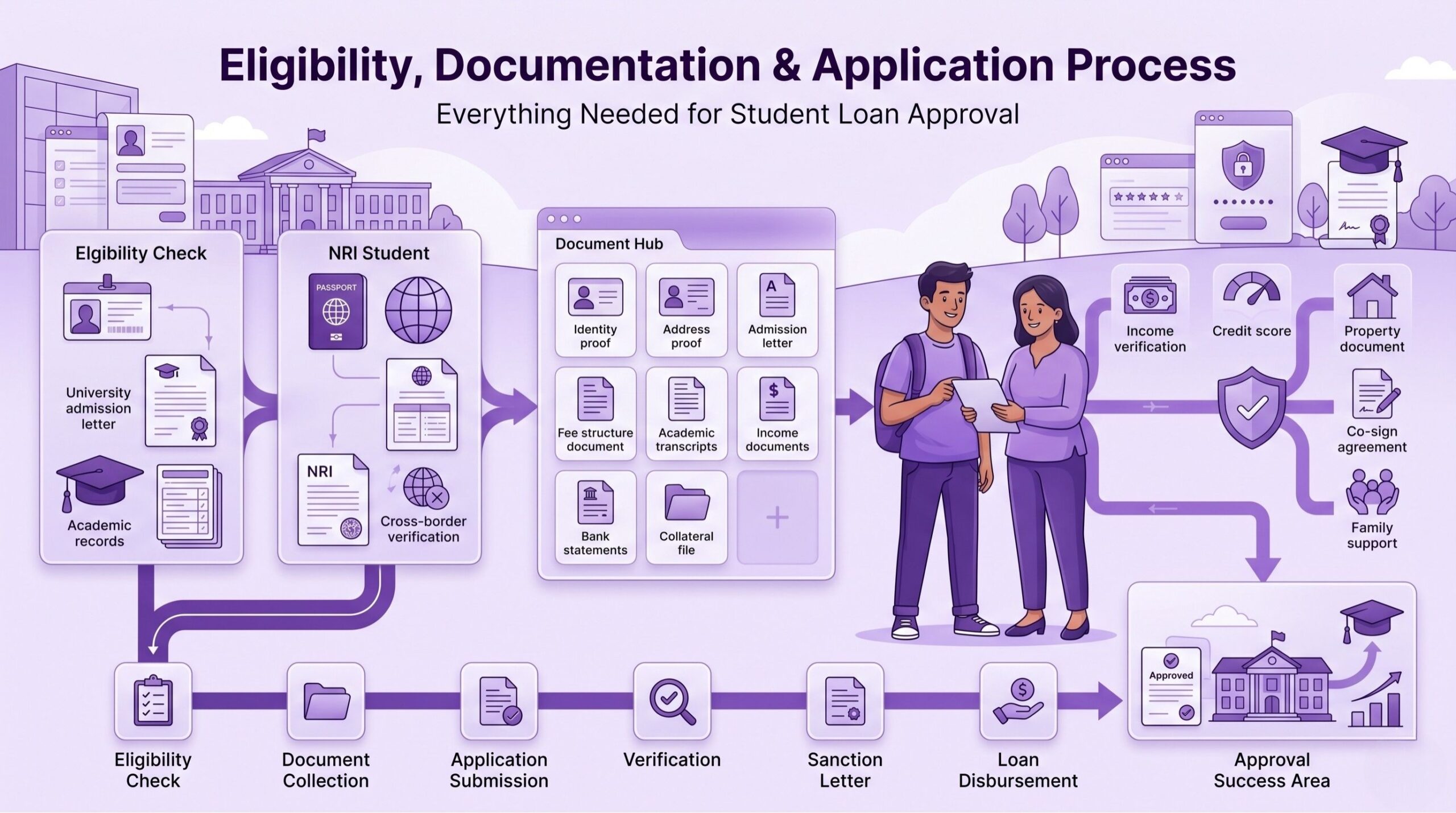

Eligibility, Documentation and Application Process

Eligibility for Indian and NRI students

Indian students:

- Enrollment in a recognised course (UG/ PG/ PhD/ diploma/ skill course).

- Co-applicant (often parent/guardian) with qualifying income and credit profile for some lenders.

- Certain special loans may also be subject to minimum academic requirements.

NRI students:

- The primary on the loan or as a co-applicant based on lender policy.

- Most lenders allow NRI parent co-borrowers, but they want an Indian resident co-borrower / Property.

- Separate KYC for foreign income sources and remittance proofs.

- List of documents (e.g.) ID, Address, Admission Proof, Fee structure, SM-5 Call letter, 10th/12th mark sheet, Co-applicant KYC, Income proofs

Core documents typically required:

These include identity proof cards such as Aadhaar, PAN, passport.

- Proof of residence: Aadhaar, passport, Utility bills

- Proof of admission: such as an Offer letter or Admission letter (or) Fee Invoice from the institute

- Course fee structure: Detailed breakup of tuition, hostel and other mandatory charges

- Education Qualifications — Marksheets & Certificates of last qualifying examination

- Co-applicant KYC: photograph, PAN, Aadhaar, passport (if NRI), signature.

- For co-applicant — salary slips for the last 3- 6 months, Form 16 for salaried; Bank statements (last 6 months or more) and ITRs (2–3 years) for self-employed.

- Collateral docs (wherever required): Docs of the residential property, title deeds, receipts of your FDR.

- Documents required for overseas study loans (when applicable): Passport and visa

Co-applicant requirements and frequently asked questions from parents

Who can be a co-applicant? Parent, legal guardian, spouse. Sometimes sibling/relative depending on lender policy

Parents often ask:

- Will my credit score be impacted? Yes — the loan appears on the co-applicant’s credit report.

- What happens if the child defaults? The co-applicant is equally liable to repay.

- Can I exit as a co-applicant later? Only with lender approval after substitution/refinance or full repayment.

- Is family property at risk? Only if pledged as collateral and default occurs.

Online & offline layers step process (Other than Vidya Lakshmi bank portals)

Step 1: Compare rates, fees, and eligibility to get a shortlist of lenders.

Step 2: (ID, admit letter, income proofs, Coll. docs if required)

Step 3: For offline application, visit the branch, or apply online via the lender portal or Vidya Lakshmi (centralised).

Step 4: Share KYC and docs — co-applicant to allow/validate.

Step 5: The lender will conduct credit and income profiling and may request a collateral valuation.

Step 6: Issuance of the sanction letter with terms; execution of the loan agreement and completion of legal formalities (stamp duty, property registration, if any).

Step 7: Disbursement of funds: Multiple tranches are sent to the institute or, as per the agreed schedule, to the borrower

How to get approved quicker and avoid rejection

- No defaults on the co-applicant’s credit report.

- File full and proper documentation — no missing pages, no non-attested copies.

- Well-explained fee structure; admission confirmation,

- Validate Property documents in advance — In-case of giving Collateral.

- Apply through Vidya Lakshmi for multiple lenders and also check status

- Ask for sanction letter with specific terms; handling fee and margin may be negotiated if required.

Interest Rates, Fees, Repayment Terms and Moratoriums

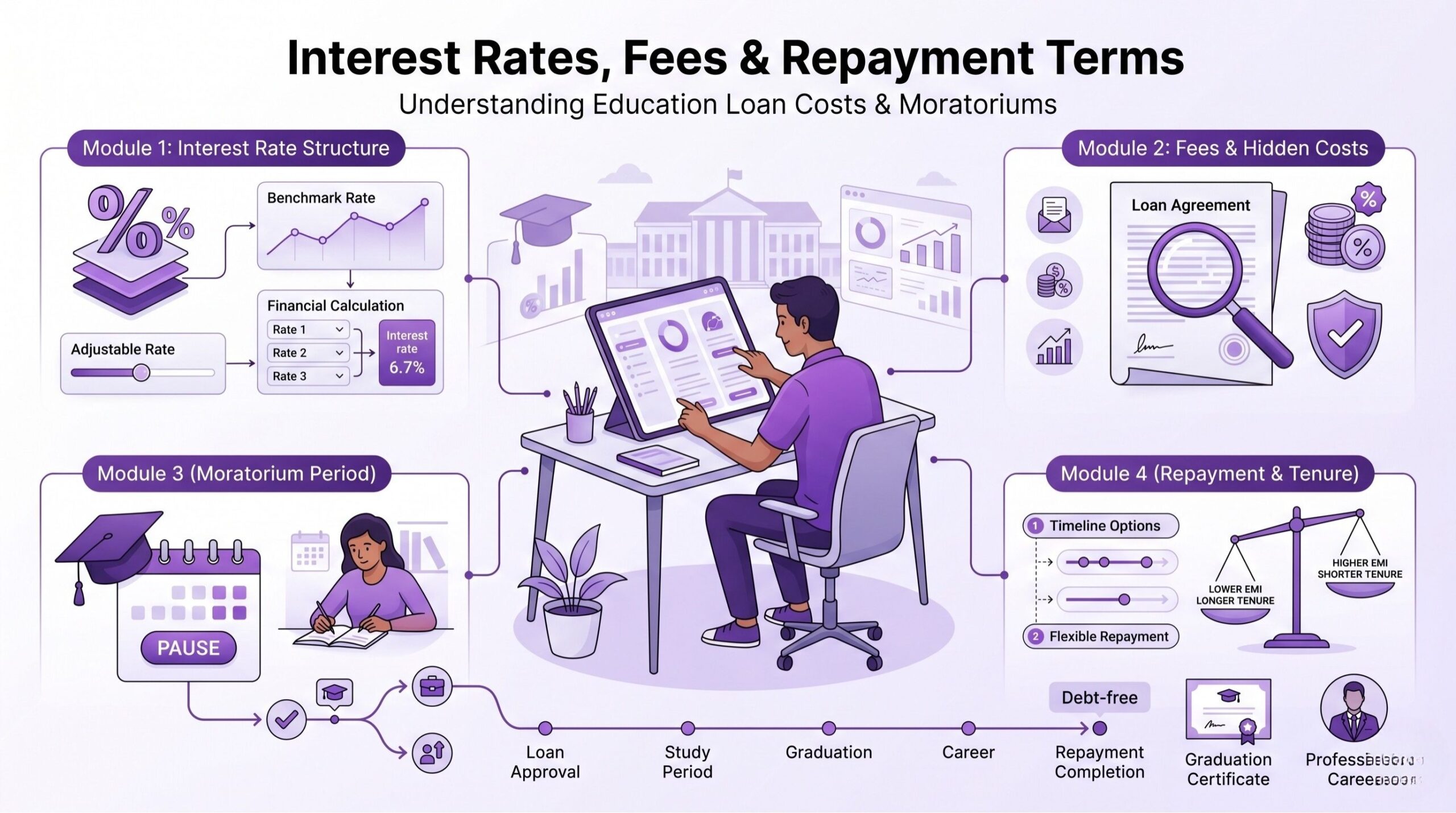

What is the structure of interest rates (base rate + spread or MCLR or external benchmarks)?

Education loan interest rates in India are normally on one of the following forms:

MCLR-linked: Lenders will keep a spread on their Marginal Cost of Funds based Lending Rate (MCLR).

External benchmark-linked: Linked to the RBI repo rate or some government bond yields + a spread; gaining traction as a disclosure measure

Base rate or internal benchmark + spread: An older system, still used by some lenders

Spread/margin: a fixed % markup added by the lender representing the risk profile, borrower creditworthiness, and collateralization. The final rate a borrower receives equals the benchmark rate plus the spread.

Typical interest rate ranges for different loan types in India (domestic UG/PG vs international)

Domestic UG/PG (secured): Historically in the 8% to 12% range, depending on lender and scheme; following the post-2023/2024 dynamics, offers can go from the standard benchmark +1–3% for better-qualified co-applicants.

Domestic unsecured or vocational loans are marginally higher, often at 10%–14%, due to increased risk.

International education loans: Higher spreads because of foreign disbursal, forex risk and larger ticket sizes—often 10%–16% based on collateral and lender.

NBFCs/private lenders: Potentially higher but may be better service or repayment flexibility

Processing fees, prepayment charges & hidden charges to look out for

And these are the basic things

Processing fee: non-refundable and a flat amount or a percentage of the loan amount, usually charged at the time of sanction; may be negotiable for big-ticket loans.

Legal/valuation fees: For collateral valuation and documentation.

Prepayment charges: As per RBI guidelines, banks typically permit prepayment/foreclosure of floating-rate education loans to specific classes without charge, while NBFCs do impose penalties—verify before signing.

Penal interest: Applicable on EMI defaults; can be large—confirm percentage.

GST: Processing fees and other service charges are subject to GST.

Caution: If the interest will be capitalised, meaning it will accumulate over a period known as a moratorium (period before the loan starts qualifying), then interest gets added to principal for every month or quarter and amortisation of hidden administrative fees or foreign exchange margin for foreign disbursals

Moratorium period: what it covers and interest rate

Typical moratorium: Course duration plus a grace period (most often 6–12 months after course completion or after an act of default), depending on the lender and scheme.

Interest during moratorium:

For a few government subsidy plans, interest paid during the moratorium helps students qualify (e.g., CSIS for PG).

In a typical commercial loan, interest is charged during the moratorium and can be capitalised (added to the principal) or deferred; both options increase overall costs.

Borrower decisions:

Pay interest during the moratorium, if possible, to prevent capitalisation and lower overall interest costs.

Check whether a moratorium is compulsory or optional in your situation, and its effect on the EMI start date.

Loan tenure options — How does it affect EMI and total cost

Maturity schedules: Education loans typically have 5–15 years of repayment after moratorium (or up to 20 for large international loans)

Impact:

Longer term = lower EMI, higher cumulative interest payment

Longer tenures: Your EMI will be lower, but lifetime interest outflow is higher.

Finding the right balance between monthly affordability and total expense is key in choosing tenure. Step-up EMIs or longer tenures with prepayment options might be the way for fresh graduates with predictable salary increases.

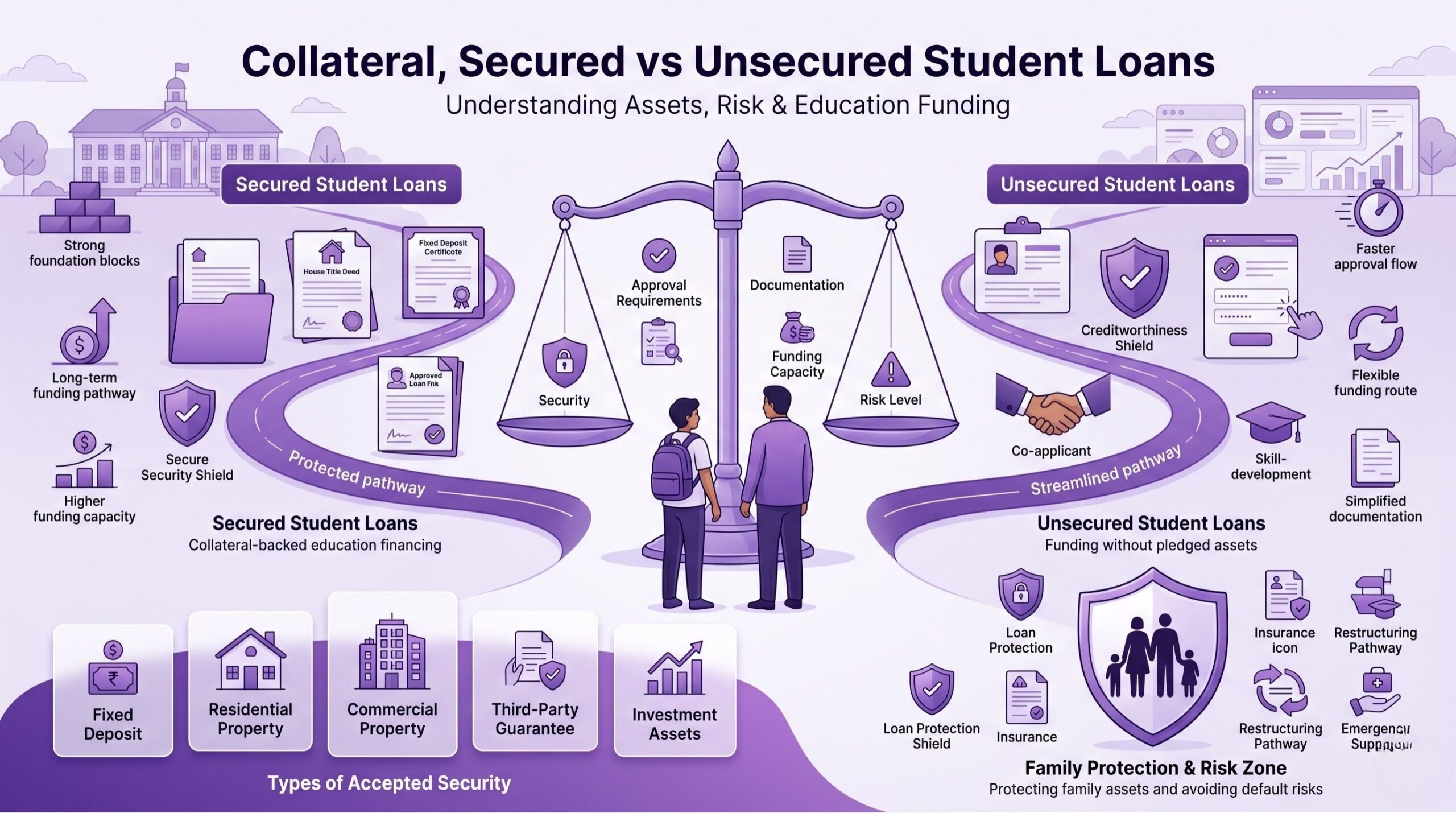

Collateral, Secured vs Unsecured Student Loans

When is collateral required? (amount thresholds, course and institute reputation)

Typically, larger loan amounts above preset limits (often INR 4–7 lakh, depending on the lender) are secured with collateral.

Top ones (Institute) easily secure higher unsecured amounts due to their best placement records.

Given the nature of these loans and the complexity of disbursal for foreign universities, collateral is the norm for international loans or MBBS programs abroad.

What type of platform collateral is accepted for use? (fixed deposits, property, third-party guarantee)

Familiar, simple bank products (such as Fixed Deposits (FDs)) Are Easier to value and widely accepted; they may be preferred for smaller top-ups.

Real estate: Title deeds to residential or commercial property; lenders check value and impose registration/stamp duty.

Third-party guarantee: Have a relative or family friend sign over their assets or act as a guarantor (Must be approved by the lender).

Securities: Stocks or mutual funds (less common, due to volatility).

Different types of collateral entail different legal and processing requirements — property-based loans require longer processing due to registration checks and the duration of the process.

Options & eligibility of unsecured loans (sponsored schemes, special product)

Unsecured education loans: Given for small amounts, skill courses or via NBFCs where a greater amount of personal risk is accepted; requires a good co-applicant with credit and also revenue.

Employer/Institution guaranteed schemes: The loans may be sponsored and secured by an institution or employer.

Government or bank sub-products: Some lenders have unsecured top-ups for standout students or certain sponsored segments.

Risks of pledging assets and how to protect family members

Risks:

- Risk of foreclosure: Default can lead to the sale/auction of pledged property.

- Legal fees and a lengthy recovery period.

Protections:

- Know the basics of foreclosure and default clauses

- Well-negotiated terms with the lender & restructuring of the loan before default occurs.

- Do not pledge asset value unless necessary and do not pledge your first family home as a matter of course.

- Look into insurance (loan protection insurance) for unexpected events such as death or critical illness of a co-applicant.

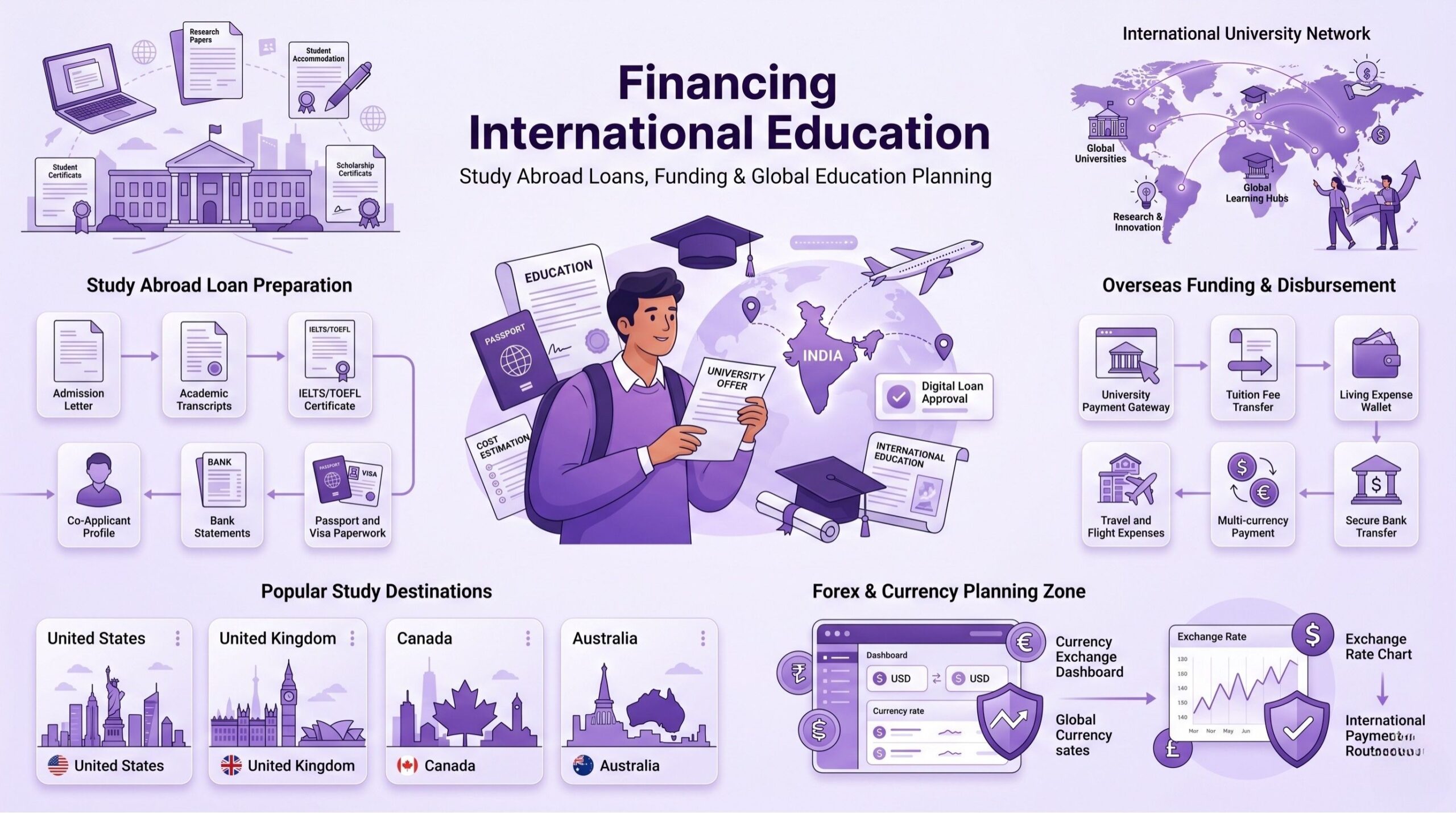

Financing International Education: Loans for Studying Abroad

Overseas course eligibility differences and top lenders for international education

Enhanced eligibility criteria: Much stronger academic qualifications, certificates, confirmed offer letters, cost estimates & budgets estimating tuition + living + travel

Co-applicant strength: While lenders look for strong co-applicants, they will consider accepting NRIs as joint applicants with due diligence of KYC

Specialised NBFCs (Avanse, Credenc, Auxilo Prime) that provide dedicated overseas education loan products, as well as major banks like SBI, HDFC, etc.

Criteria: Some lenders require collateral for higher loan amounts, while others offer unsecured or partially collateralised funding, depending on the destination/course or ROI.

Study Abroad Specific Documents (Offer Letters, Cost of Living, Bank Balance, Currency Conversion)

- Offer/Admission letter: Required. Contains tuition and acceptance terms

- Fee timetable and payment cut-off dates — comprehensive bill from university

- The cost-of-living calculation will include housing, provisions, coverage, and contingency.

- Bank statements for co-applicant: Often 12 months to demonstrate stability and ability to service EMIs

- Passport and visa paperwork: To facilitate disbursement and processing of the loan.

- Foreign university pre-admission tests & credentials: IELTS/TOEFL scores, transcripts

- Currency/FX Proof – Some of the lenders ask for conversion estimates in foreign currency and may also request forex account details.

Concerns related to Forex, Conversion Hedge and Basics of Hedging for Indians

Disbursal currency: Banks usually make disbursals to foreign universities in foreign currency or to students’ Rupee accounts and expect the beneficiary to convert. Exchange rate margins and banking fees are applicable

Timings: The effective cost of currency can be affected by volatility, so shooting from the hip would mean planning disbursements when the rate is favourable.

Hedging basics:

Forward contracts: Lock in a future exchange rate (available only to businesses and high-value disbursements).

Forward sells: Lock rates while they are reasonable, and if your long-term disbursals (sell) payments span long periods of time — utilise staggered loads to normalise again.

Lender support: multiple currencies or forex tie-ups — ask your lender.

Components of conditional disbursals, living expenses and tie-ups with foreign universities

Conditional disbursals: The lenders may disburse the tuition fees directly to the university and release living expenses in tranches after the applicant has arrived abroad, or upon submission of hostel bills and airfare receipts.

Living expense coverage: Usually on a per-lender basis; you may need to provide post-arrival receipts or bank statements if more than 1 tranche is disbursed.

University tie-ups: Some lenders have direct payment agreements with larger universities, which can result in faster settlement of tuition balances while reducing the amount the student is responsible for.

Example case: common structure of loan masters in the US / UK / Australia / Canada or MBBS abroad

US Masters (1–2 Years): USD 30k & 80 Lakh, with Tuition Fee: Lenders cover up to 60 Lakh tuition fee and Living Expenses, with a moratorium of about 2–3 Years and a tenure of approx. 10 years. Amounts > INR 20 lakh: Collateral usually needed unless the co-applicant’s credit is exceptional.

UK Masters (1 year): Expensive tuition but shorter course duration. Moratorium until 6–12 months after the course. For many years, lenders have funded full tuition, plus a reasonable living allowance, directly to the institution of higher education. Smaller tenure means minimising interest during the moratorium.

Australia/Canada (24 months): Tuition and living expenses with staged disbursements; Income of co-applicant is scrutinised very closely for visa compliance.

MBBS Abroad: Super high ticket sizes (tuition + hostel very often 30–70 lakh+). Almost always comes with collateral and property documents; lenders mainly lend to recognised medical universities that provide placement support.

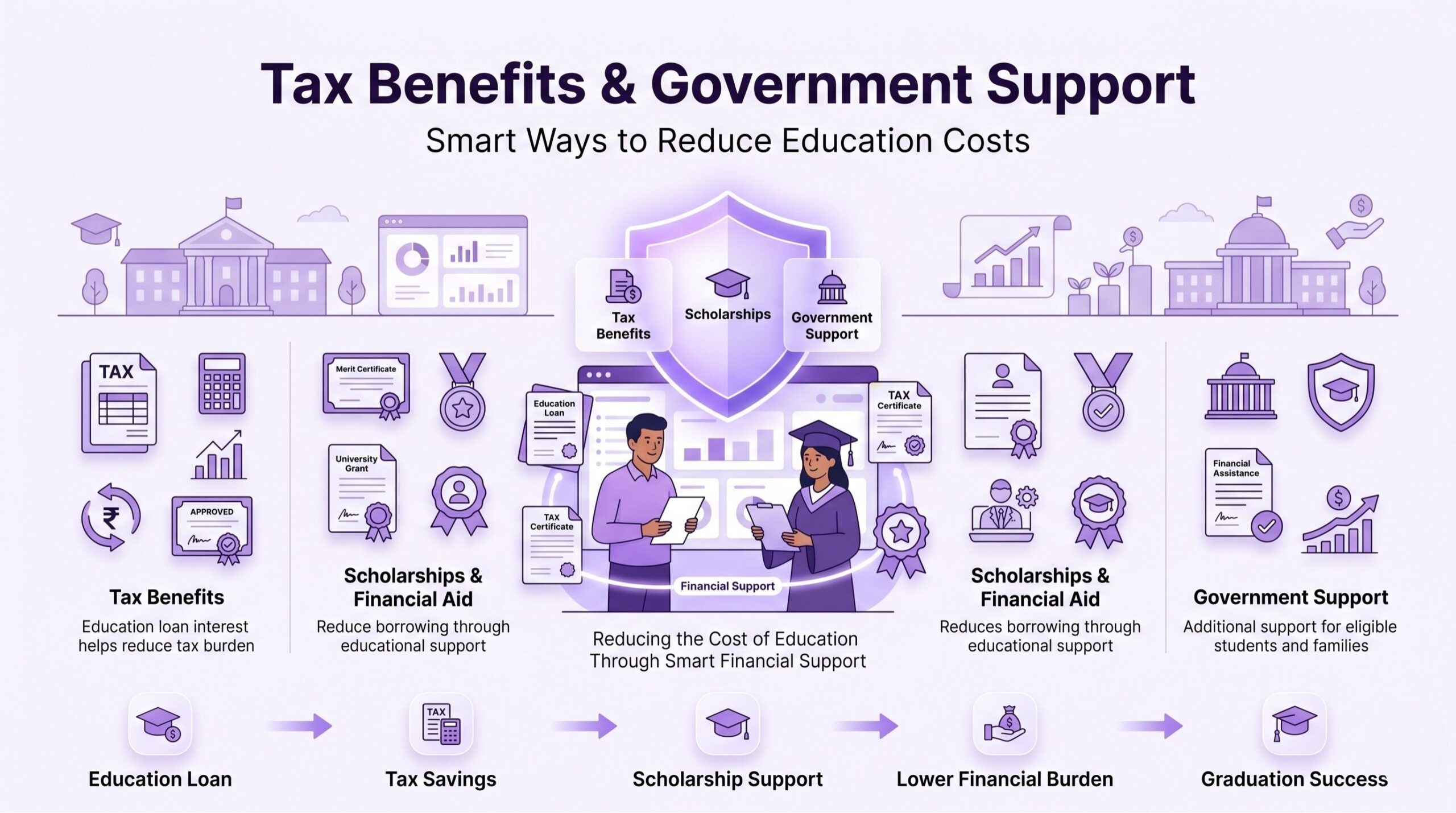

Tax Benefits, Subsidies and Government Support for Students and Parents

Tax-deductible interest and taxpayers are eligible for two loans (80E, etc.)

Section 80E: The interest paid on an education loan by the borrower (generally the parent or student) can be claimed as a deduction from taxable income for a maximum of 8 assessment years or the actual payment of interest, whichever is earlier. Under 80E, principal repayment is not deducted.

Principal repayment: Unlike home loans, which offer benefits under section 80C, the principal repayment on education loans is not deductible as an expense for income tax purposes.

Interest subsidy schemes for economically weaker students: (Eligibility and Application)

CSIS(Central Sector Interest Subsidy) & some state schemes from time to time for certain courses or income-less than 4.5/6 lacs (interest-free during moratorium period)

Application: through lender or Vidya Lakshmi (documentation of eligibility & income required)

Scholarships at the state and central levels that (truly) lighten the loan burden

There are many scholarships available for both merit- and need-based students; central scholarships (e.g., merit-cum-means) plus state scholarships can be availed together with loans to reduce the payment amount.

Scholarships at the institutional level: Many universities will waive part of your fee, as well as assistantships or stipends for research/TA positions; these minimise borrowing.

How parents can optimise taxes while paying down student loans

- Interest payments are classified under the 80E deduction—the taxpayer benefited from most of the plan payments.

- Use the loan’s repayment periods to align with income cycles and file interest claims in the appropriate AY.

- Keep on file records of interest paid and lender certificates necessary for tax filing.

Repayment Strategies, EMI Management and Early Repayment

Select the type of repayment plan (step-up, step-down, fixed EMI, flexible EMI)

Fixed EMI: This stable, unified monthly value means predictable budgeting and easier repayment if you stay disciplined.

Step-Up EMI: Lower EMIs (equated monthly instalments) at first that increase over a period of time as the expected salary increases—ideal for freshers with an obvious career hike in sight.

Step-down EMI/balloon repayment: Higher principal amortisation in the initial years reduces interest burden; balloon payments mean a lump sum is due at the end.

Moratorium on EMI: Provides for a moratorium period that could temporarily lower EMIs or obligate only interest payments to reduce monthly outgo.

Choose by:

- Step-up if you expect your salary to rise sharply.

- Fixed EMIs offer predictability, while step-up can become a burden if salary rises more slowly than anticipated—risk tolerance.

Moneytips, Budgets, Save-up, Cashflow tips for fresh graduates in India

- Develop a conservative budget: 30–40% of net salary as a safe disposable income, and EMIs may be 20–30%, if at all.

- Prepare an emergency fund (3–6 months of outflows before aggressive prepayment)

- Automate payments: Use auto-debit to ensure timely payment of EMIs; otherwise, your credit score could suffer.

- Side hustle: Freelancing, tutoring or part-time work to pay EMI

- Pay off High-Cost Debt First — pay off other debts that will charge more interest than that education loan first.

Prepayment and foreclosure rules: when is it justifiable

Foreclosure makes sense when:

If you have the extra cash to repay early and prepayment penalties are low or none.

Foreclosure saves more than interest lost on alternative investments.

Verify with your lender whether you can prepay: lenders are often lenient with floating-rate education loans and do not levy penalties for foreclosure, but NBFCs are not.

Partial Prepayment: You can either reduce the EMIs (Equated monthly instalments) or shorten your loan tenure, depending on your financial goals.

Addressing salary gaps, deferment options & negotiating with lenders

If salary gaps occur:

Question them in advance so you don’t get penalised; Lenders usually grant short moratoriums, EMI holiday or loan restructuring

Share the updated income proofs to re-negotiate your EMI or tenor.

Negotiation tips:

- Provide valid income projections or letters of job offer.

- Intermittent relief where you could request step-down or interest-only periods

- Indian banking grievance redressal regulatory mechanism: Apply through the Vidya Lakshmi grievance options and seek help from a banking ombudsman if needed.

Use of balance transfer/refinancing to reduce interest burden

Balance transfer: Transfer existing debt to a bank with lower interest or other favourable conditions. Include processing fees, leftover tenure and break-even point.

Refinancing: use a new loan (may involve different collateral or a co-applicant) to settle the existing loan, with a reduced EMI and total interest.

When to consider:

- Significant rate differences.

- Improved customer support/ lenient repayment.

- Informed credit profile of co-client loosening up spreads.

- Estimate on total cost (for both, prepayment penalties & transfer fees) and payback time.

Dealing with Defaults, Restructuring and Credit Score Impact

Impact of missed EMIs on CIBIL and other Indian credit bureaus

- Failure to make payments results in reports to credit bureaus (CIBIL, Equifax, Experian), lowering credit scores.

- After a few days of overdue defaults, banks classify them as NPAs (non-performing assets) and initiate recovery processes.

- Effects: impaired access to future loans (home/auto/work), higher interest rates, difficulty obtaining credit cards.

How lenders approach restructuring and one-time settlements

Restructuring: Lenders may consider loan restructuring — extending the tenure, making the initial few months interest-only, or changing the repayment pattern so that the borrower does not have to default.

One-time settlement (OTS): Lender provides a percentage of the total amount outstanding as a lump-sum settlement — usually affects your credit history and future eligibility.

Strategy: If a borrower has credible repayment capacity, lenders would restructure sooner than pursue legal recovery.

Notices to be issued, process of recovery and rights of the borrower under Indian law

Legal process: Bank issues notices, can also sue and initiate legal proceedings under the SARFAESI Act (for secured loans) or approach Debt Recovery Tribunals. Civil suits exist for unsecured loans.

Borrower rights:

- Right to be noticed and heard.

- Right to request restructuring and demonstrate evidence of hardship.

- Protection against coercive recovery process—Approach Banking ombudsman

- Take control- begin negotiating with the lender as soon as possible; get legal or financial help before lawsuits are filed.

How To Rehabilitate A Credit Score After Default

- Settling or Paying Off debts

- Ask the lender to change status after settlement and issue an NOC.

- Lay out never late on any other credit moving ahead.

- Check the credit report periodically and correct any errors.

- Convert to safe credit (e.g., a small loan-backed FD) and pay on time to rebuild a healthy track record.

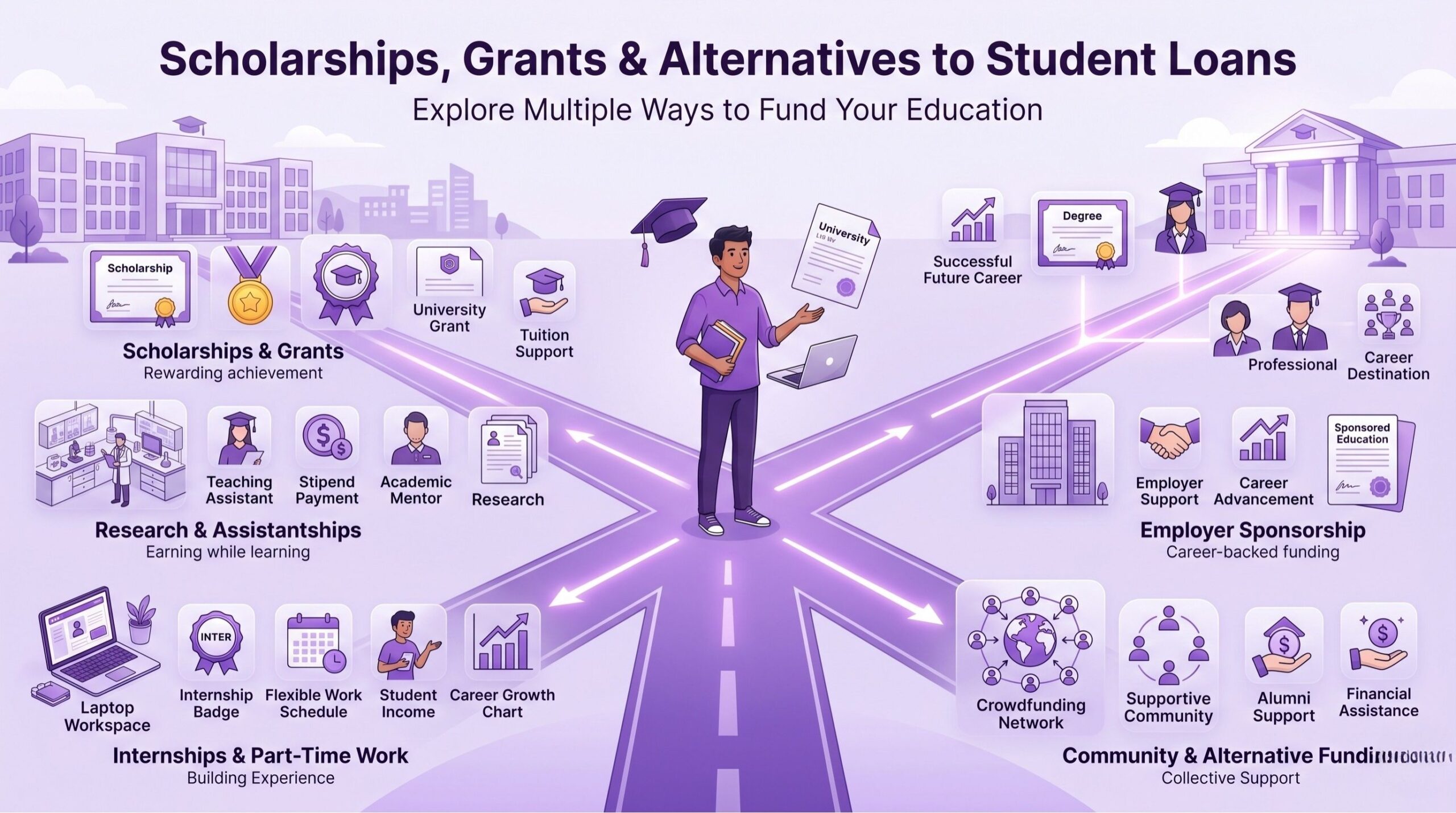

Scholarships, Grants, and Alternatives to Student Loans

The scholarships given by central and state governments that are relevant for Indian students

Central scholarships: Merit-cum-means, national fellowship schemes, scheme-specific awards for SC/ST/OBC/Minorities and academically weaker sections.

State scholarships: These vary by state, but many states offer excellent tuition assistance and stipends for domiciled students.

Application: Typically through centralized portals or state education departments—early applications are recommended to mitigate the use of loans.

Scholarships, University level: merit-based scholarship, need-based scholarship

Based on Financial Need: Determined by how much assistance a student needs to pay for school.

Research/TA/RA positions provide stipends and tuition remission—fairly common in PG and Ph.D. programs as a form of financial aid (thus need-based/assistantships).

College tie-ins: Many colleges offer sponsorships or fee-waiver initiatives for strong students.

Education crowdfunding, income-share agreements (ISAs) and employer sponsorships

Crowdfunding: Students can crowdfund their partial funding needs through a platform (i.e., useful for niche needs, fees, and no guaranteed outcome).

ISAs (Income-Share Agreements): Have Not Yet Hit India and are in R&D — students get money for an agreed-upon % of their future income for a period. Good for high-ROI courses, but long-term payout caps

Employer Sponsored: Corporates may sponsor courses but with a bond period or partial payment of course fees [good for working professionals looking to climb the hierarchy)

Employment, internships and work-study in India and abroad| A substitute for the loan

India: Several colleges offer part-time assistantships or industry internships that can help defray living costs.

Abroad: Student work permissions vary by country—Canada and Australia allow significant part-time work; the US has stricter on-campus/off-campus rules.

Strategy: Earn a part-time income and work out scholarships to minimize the size of loans and therefore EMIs.

Practical Checklist: Applying, Managing, and Closing a Student Loan

A checklist of things for students and parents to do before applying

- Letter of acceptance (admission confirmed fee structure and offer letter)

- Narrow it down to 2–3 lenders and look for interest rates, fees, and moratorium.

- Co-applicant credentials, credit history check.

- Lay out property papers if collateral is required and prepare report/property hold details.

- Create an account on the Vidya Lakshmi portal for tracking multiple applications and scholarships

Checklist for disbursal and utilization (fee payments, installments to institute, forex documentation)

- Make sure the sanction letter specifies the disbursal rule (direct to the institute or to the borrower).

- Retain fee receipts and create communication within that tranche of disbursal.

- For abroad studies: Keep forex receipts, visas, passports & arrival proofs for release of the next tranche.

- Log all communications with the bank and preserve evidence of disbursal through bank statements.

Mid-loan check: oversight of interest, statements & correspondence

- Verify interest calculations, and EMI debits from bank statements regularly;

- Obtain the annual interest certificates to be filed with your tax return (Section 80E)

- Maintain a good record of this loan agreement, including all correspondence; update contact details and income information if they change.

- Review CIBIL and credit reports once a year.

Finalizing the loan: Documents needed, NOC, CIBIL update

- Acquire the final settlement receipt and NOC (No Objection Certificate) from the lender after foreclosure or the last EMI payment.

- Ask the lender to report to the credit bureaus if any are flagged for the payment-free period.

- Gather genuine litigation reports, e.g., title deeds/FDs, and verify at higher levels of repayment documentation.

- Keep evidence of closure for reconciliation purposes.